|

August 2005 Incentives Deal of the Month from Site Selection's exclusive New Plant database |

|

|

August 2005 Incentives Deal of the Month from Site Selection's exclusive New Plant database |

|

|

LOOKING FOR A PREVIOUS STORY? CHECK THE

ARCHIVE.

Trumping Cuno

Ohio's tax reform package

could give commerce back its claws.

In the same state whence came the infamous Cuno v. DaimlerChrysler incentives decision from the U.S. Sixth Circuit Court of Appeals, July 1 saw the debut of sweeping tax reform that seeks to immediately sweep away some of that decision's sour aftertaste.

©2005 Conway Data, Inc. All rights

reserved. Data is from many sources and is not warranted to be

accurate or current.Part of the state's biennial budget bill, the reform package includes the following highlights:

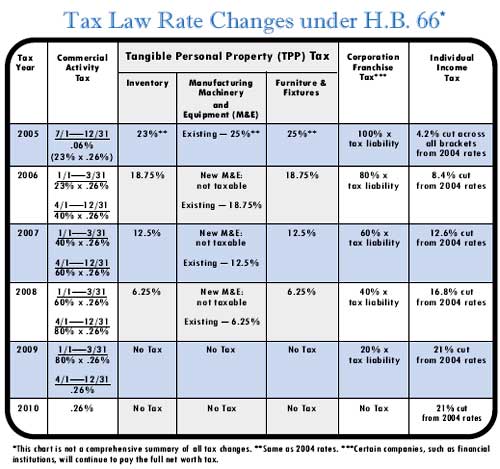

The new tax scheme applies to receipts over $1 million, and is set at a rate of 0.26 percent. New machinery and equipment purchased since July 1, 2005, is immediately exempt from personal property tax. The corporation franchise tax will phase out over five years at the rate of 20 percent annually, while the tangible personal property tax on most businesses' inventory, manufacturing machinery and equipment, furniture and fixtures will phase out over four years at about 25 percent annually beginning in tax year 2006, says the Ohio Dept. of Taxation. Among the provisions of the legislation is the levying of the CAT on those entities with substantial nexus in the state. That is defined by its "bright line presence." According to the letter of the law, a taxpayer has a bright line presence in the state if it a) has property or payroll in the state valued at at least $50,000; b) has gross receipts of at least $500,000; c) has at least 25 percent of its total property, payroll or sales in the state; or d) is domiciled in Ohio.

Also part of the new package is elimination of the 10-percent property tax rollback on most commercial and industrial real property. That rollback remains for agricultural and residential property. Other revenue sources? The state's permanent sales and use tax, as of July 1, is now up to 5.5 percent. Also, Ohio's cigarette excise tax just leaped from 2.75 cents per cigarette to 6.25 cents per cigarette. The new tax program is thought to be to the benefit of larger corporations but to the detriment of some high-volume, low-margin businesses like grocers and other retailers.

Fast Relief

The ink was barely dry on the new bill when Norfolk Southern Corp. reported that, because of the new tax legislation, the company's second-quarter reported net income would increase by approximately $95 million, or $0.23 per diluted share. The railroad operates an extensive rail and facility network throughout the state, employing 4,107 people with a total payroll of some $192.1 million. The company just moved forward with an intermodal investment at Rickenbacker International Airport in Columbus. Mittal Steel's second-quarter financials reported an immediate $20-million tax credit because of the changes. And Anheuser-Busch reported a $7.2 million reduction in deferred income taxes.

In Lorain, meanwhile, according to statements sent to the city's Morning-Journal newspaper, officials with Industrial CH, S.A. de C.V., the new Mexican owner of the Republic Engineered Products steel mill facilities there, said that while the company hasn't made a final decision about its investment plans for the complex, the tax reform "should have a positive influence on the business investment climate in Ohio." Later in July, Taft gave credit to the new package for improving the state's business climate enough to attract expansion like that from aerospace and defense company LORD Corp., which is investing $3.8 million in a 30-job expansion in Dayton. In competition with Pennsylvania for the project, Ohio gave the company a direct loan, a job creation tax credit and a training program grant as part of its incentive package. "Thanks to our recently enacted tax reform plan, Ohio is now an even better place to locate and expand a business," said Taft. "With our enhanced business climate and the presence of world-class companies like LORD Corporation, we are sending a clear, strong signal that Ohio Means Business." The outlook indeed may be promising for manufacturers. Detailed analysis of the law from the law firm Bricker & Eckler LLP reports, "Many manufacturers should see a reduction in their overall business tax burden as a result of the tax

In addition, receipts from transactions between related entities that are part of a consolidated taxpayer (e.g. a manufacturing company) will be excluded from taxation, and if that consolidated group includes a foreign corporation, all or none of the group's foreign corporations may be included in the group. Receipts from goods sold into certain foreign trade zones will be excluded as well. There are still plenty of credits to be had: the jobs creation tax credit, the jobs retention tax credit and qualified R&D and R&D loan payment credits. Also, net operating loss carry-forwards and other deferred tax assets in excess of $50 million are now eligible for a non-refundable credit. According to Bricker & Eckler, "The credit is based on amounts reflected on the taxpayer's books and records as of the end of its taxable year ending in 2004. Up to 10 percent of the credit may be claimed against up to one-half of the CAT liability for tax years between 2010 and 2019; from 2020 through 2029, up to 100 percent of the credit may be claimed against the first one-half of the CAT liability."

Next Battles Enjoined

The central relief of the new scheme is that the manufacturing machinery and equipment and corporate franchise taxes at the center of the Cuno case will no longer be there, so there's no danger of having a credit toward them declared illegal.

The schedule calls the listing percentage for manufacturing machinery to remain at 25 percent for 2005, then go to 18.75 percent in 2006, 12.5 percent in 2007, 6.25 percent in 2008, and nada after that. Accordingly, the aforementioned credit is limited to equipment acquired before June 30, 2005, and installed before June 30, 2006. New credits and carry-forwards may not be applied for any taxable year ending after June 30, 2005. Significantly, a new grant that was intended to take the place of the credit was vetoed by the governor when he signed the bill, because of the pending federal litigation. And how is that litigation pending lately? In June, DaimlerChrysler and the State of Ohio filed petitions for a writ of certioriari, in essence asking the U.S. Supreme Court to consider reviewing the 6th Circuit Court of Appeals' decision regarding an investment tax credit against the state's now-disappearing corporate franchise tax. Meanwhile, looking for more, Cuno and fellow plaintiffs have also filed for a writ of certiorari, because the 6th Circuit Court of Appeals actually upheld the constitutionality of an exemption from the personal property tax imposed by Ohio municipalities. Reply briefs to all petitions were due today, Aug. 18. Meanwhile, even as he battles ethics charges, Gov. Taft has another cause to champion. The Ohio legislature just passed his "Jobs for Ohio" bond initiative, allowing the measure to be placed on the state's November ballot. Among the measures in the $2-billion initiative — a re-branding of the state's Third Frontier program — are steps to improve community business infrastructure, support high-tech R&D and create large shovel-ready sites for business development. But a major amendment in the package calls for limitations in the definition of "public purpose" in site development, in order to avoid eminent domain actions supported by the recent Kelo decision from the Supreme Court. Seems you can't walk around the corner without bumping into a legal ruling. But some Ohio businesses would say that, via the tax reform, at least some solid ground has already been prepared.

|

||||||||||