In conjunction with Site Selection’s July 2026 publication of “The Border Is Not One Market” by Avison Young Senior Director, Industrial Corporate Services Carl Quesinberry, Editor in Chief Adam Bruns spoke in June with Quesinberry and Avison Young National Industrial Market Intelligence Director Peter Kroner about the location and policy dynamics influencing location decisions along the border corridor. The Q&A below is an edited excerpt of that conversation.

Of note: Personal border crossings can be as good an indicator as any of a region on the rise. “I only crossed the border twice in 2025,” Quesinberry said. “I’ve done it four times in 2026, and I have three more scheduled visits … I wouldn’t be surprised if it’s 12 by the end of the year.” — Ed.

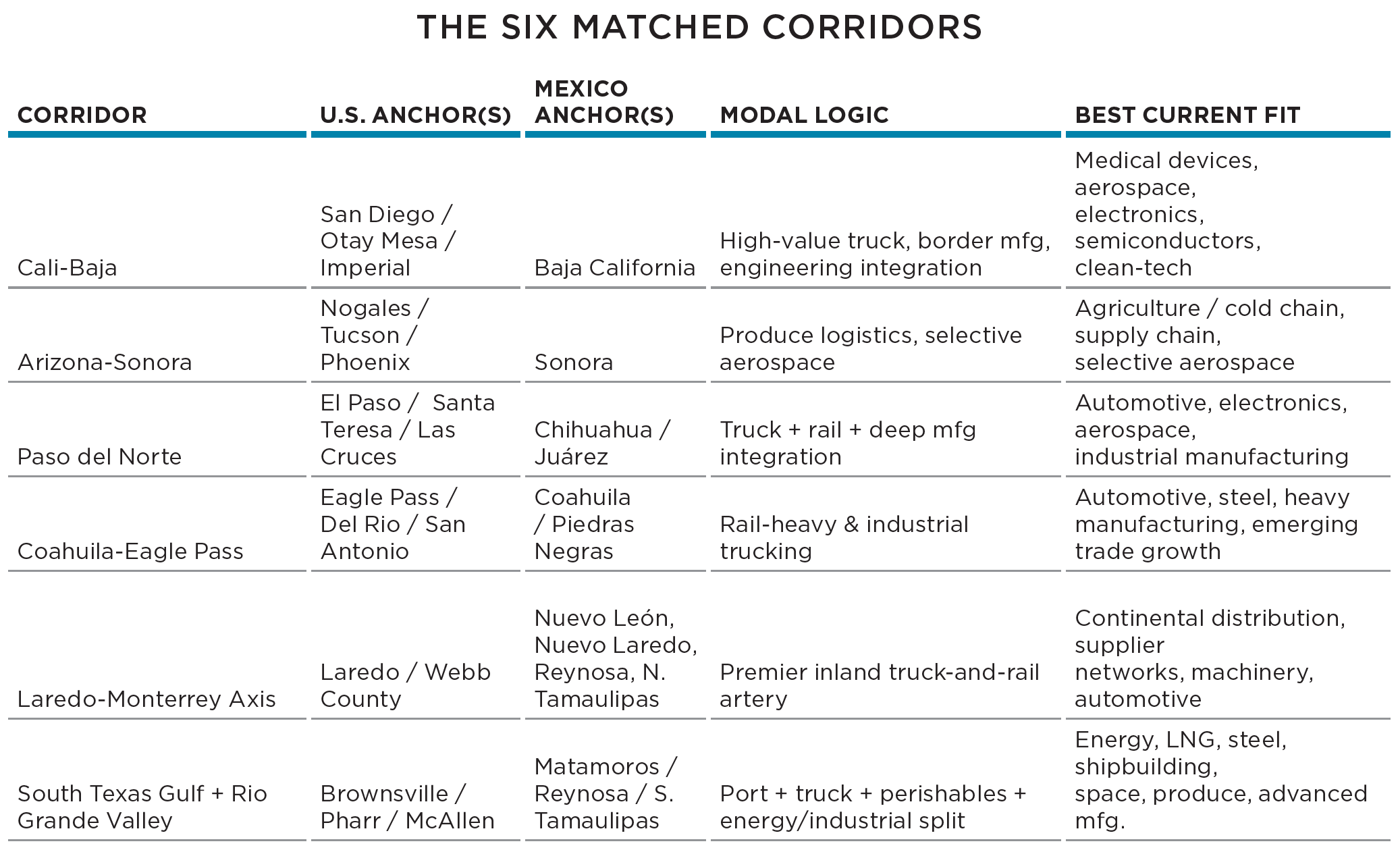

Site Selection: What are your thoughts about how USMCA negotiations need to play out to best benefit the six binational regions you lay out in your border report?

Carl Quesinberry: The addition and deployment of capital, regardless of which side of the border you’re on, it can’t be this football. We need some basic things we can count on, that make people more comfortable in making those decisions to deploy capital on either side. I don’t want to say “certainty,” because policy is always in flux, but more tightly knitted than today.

Peter Kroner: We track the eight largest ports and two largest Mexican ports. Volumes ever since the 2023 merger of Canadian Pacific and Kansas City Southern and that come in on the Pacific side of Mexico have been elevated since 2018. We are also seeing this in Houston … the Texas Triangle is really dominating. Volumes are up almost 60% since 2018 from the Port of Houston. Close to 100% growth at the Mexican Pacific ports. KCS had built the largest port, but there’s still a gap, with a 45-minute to one-hour drive. To really reap all the benefits of that investment, there has to be Class I branching there to really see a huge surge of volumes that go across the border. Also we’ve seen a lot of investment on the truck side around Laredo. We’ve seen those truck lines continue to increase. It’s positive for relations between Mexico and the U.S. There is a handful of FIBRAs [Mexico’s equivalent to a REIT] down there holding the vast majority of the product. Mexico articulated that the cost savings between them and China isn’t there anymore. Now with the One Big Beautiful Bill Act [OBBBA] and qualified production property and qualified improved property for manufacturing that is writing off the U.S. for manufacturing from Jan. 1, 2029, a lot of the advantages Mexico had, it’s making folks that didn’t pull the trigger on Mexican locations reconsider the United States. Not to mention rapid depreciation of equipment on day one.

Give credit where it’s due under the Biden Administration — it surged chips, etc. But only a handful of industries are benefiting. With this provision in the Big Beautiful Bill, it’s agnostic about investment. We’re helping an $8 million expansion that takes all the inputs, runs assembly lines and 80% of their costs are covered by the Big Beautiful Bill. [Companies are] reconsidering the math and equations in going elsewhere vs. coming to the U.S. … I still think there is a lot of complementarity between good neighbors. What’s good for both of our countries is good for North America.

Carl Quesinberry: There is a mishmash of determinants and drivers. The policy issues, that’s today’s flavor of the week. Getting that to where there’s an equitable dynamic between both countries will really serve us well. From the determinant standpoint, railway infrastructure and modernization of the ports are critical factors that will yield generational benefits. I would argue that among those six corridors along the border, there lies opportunity. Could there be seven, eight, nine or 10 corridors? You could do so with optimization with the mindset of the flow of goods back and forth.

Given confusing or punitive signals from Washington when it comes to international trade and commerce, many have pointed to sub-national diplomacy as the way to go for regions wishing to work directly with foreign countries, cities and companies. Which of the six bi-national regions on the border are the furthest along in cementing these connections?

Carl Quesinberry: I have not seen any take both sides of the border and do it well. We’re human and take our own interests. But there is a harmonious conversation to have there relative to components and integrated supply chain. And derisking — maybe I need to leverage labor arbitrage on one side, and production on the other side. As for a common singular voice, I haven’t seen it done well yet. I’ve seen a lot of fiefdoms. COSTEP does a very good job, and covers almost all the border regions from Brownsville up to Laredo. Laredo Nuevo does a very good job. Chihuahua One. And Monterrey has a big organization. All are fiercely competitive. But even the second prize is a big prize in an integrated supply chain. If somebody gets the production facility, the ancillary facilities that support that are a big one as well.

Chart courtesy of Avison Young

Antonio Garza told us in our May issue that the real challenge now for site selection in Mexico “is finding the right spots where the energy grid and water infrastructure can actually keep up with new demand.” Which of the border markets is doing the best at this?

Carl Quesinberry: The fiber is easier to address. 144-strand fiber is the least amount of fiber when you start talking about data centers. As you expand that conversation and the connectivity through fiber, those lines need to be much more robust. I can’t speak to how that’s going from one side of the border to another, but I can speak to how those border corridors aligned with a service provider to put those higher fiber concentrations in are going to put themselves at a competitive advantage. I’ve seen one location do that: Laredo.

Peter Kroner: The Trump administration last summer approved that $10 billion semi-automated freight corridor between Monterrey, Nuevo Leon, and Laredo, with 150 miles of elevated bridge that is designated for freight. It’s a $10 billion, privately funded project. We see what the investment in port of entry in Laredo has done for TEU volumes. Granted it was launched during COVID-19. But before and after, the commercial border crossings just surged. This is going to build up not just the Mexican feeder markets, but Laredo, San Antonio and Austin ultimately. With everything that has happened with Houston’s development and growth, there’s a mega-regional cluster that facilitates global trade and Texas domestic trade all within 150 miles of each other.

There is a lot of investment in fiber, and water commitments from these different municipalities. Texas has the advantage of having its own grid. There’s no cap on the natural gas side of things in terms of power. They’re putting them up, unlike California or Illinois. I know Texas is committing to new power plants from a variety of sources. That’s a big bonus right now.

Also, with the water commitments for this new generation of hyperscaler, it’s like a pool: Fill it once and there’s no evaporation. The market is dictating there isn’t cheap water anymore. In Texas, Mexico and California, these are big barriers to being able to roll out the growth and accelerated buildout they need.

Carl Quesinberry: I think there’s a real opportunity for Mexico relative to this data center renaissance, particularly as behind the meter is becoming the way to go for power generation. It’s predominantly better in the U.S. than in Mexico. If you can control your own island and you’re not tethered to production, I see vast data center expansion in Mexico.

Peter Kroner: With the Avison Young U.S. Manufacturing Investment Tracker, we’re tracking all these investments since the OBBBA was launched. We’re tracking $3.4 trillion worth of manufacturing projects, new or expansions. There is a lot of it going into Texas, California and Arizona. We’re not seeing the spin dollar happen yet. But you need to pit different teams of incentives against each other. It’s about year into that process, so we expect more shovels in the dirt the second half of this year.

How will Otay Mesa East benefit an already surging Cali-Baja region?

Carl Quesinberry: If more growth is possible, more growth. I think energy will be the big limiter there, but maybe not. The technological advances they’ve made in that cross-border exchange I believe is the model, a blueprint of what can be, and how successful it can be, with an optimal exchange for flow of goods back and forth. I think it’s not prudent to continue to try to push throughput through really constrained chokepoints. I would propose scrapping and starting anew — keeping the throughput going but create a replacement thoroughfare. There are only two bridges in all of the cross-border corridor that can handle hazardous goods. That’s just mind-blowing to me.

Which of the six border markets demonstrate the strongest alignment in terms of cross-border collaboration between counties and cities on the U.S. side and Mexico side? Share a project-based example of such collaboration that you’ve observed firsthand.

Carl Quesinberry: There’s an automotive steel plate punching manufacturer on this side, while on that side the labor arbitrage isn’t nearly as robust as it once was. Depending on where you are in Mexico, your energy prices can be higher than other places in the U.S. Vertical integration of the supply chain came into play. We bifurcated operations mostly because of environmental regulations being less stringent than the other. That was Monterrey-Laredo. Again, these are 20- to 40-year life cycle costs with significant capex on the front end. So these policy decisions become even more crucial in being stable, putting that element of unknown into the equation and solving for that risk premium.

The calculus is that the saber rattling is probably over relative to trade conversations and things will settle down even more so. A higher degree of predictability will happen. The American consumer is what every company wants to solve for. Given energy, labor costs and the drive toward automation, it pencils out standing up new operations in Mexico or the U.S. to serve the market.