Plus: Site Selection Insights from Industry Experts

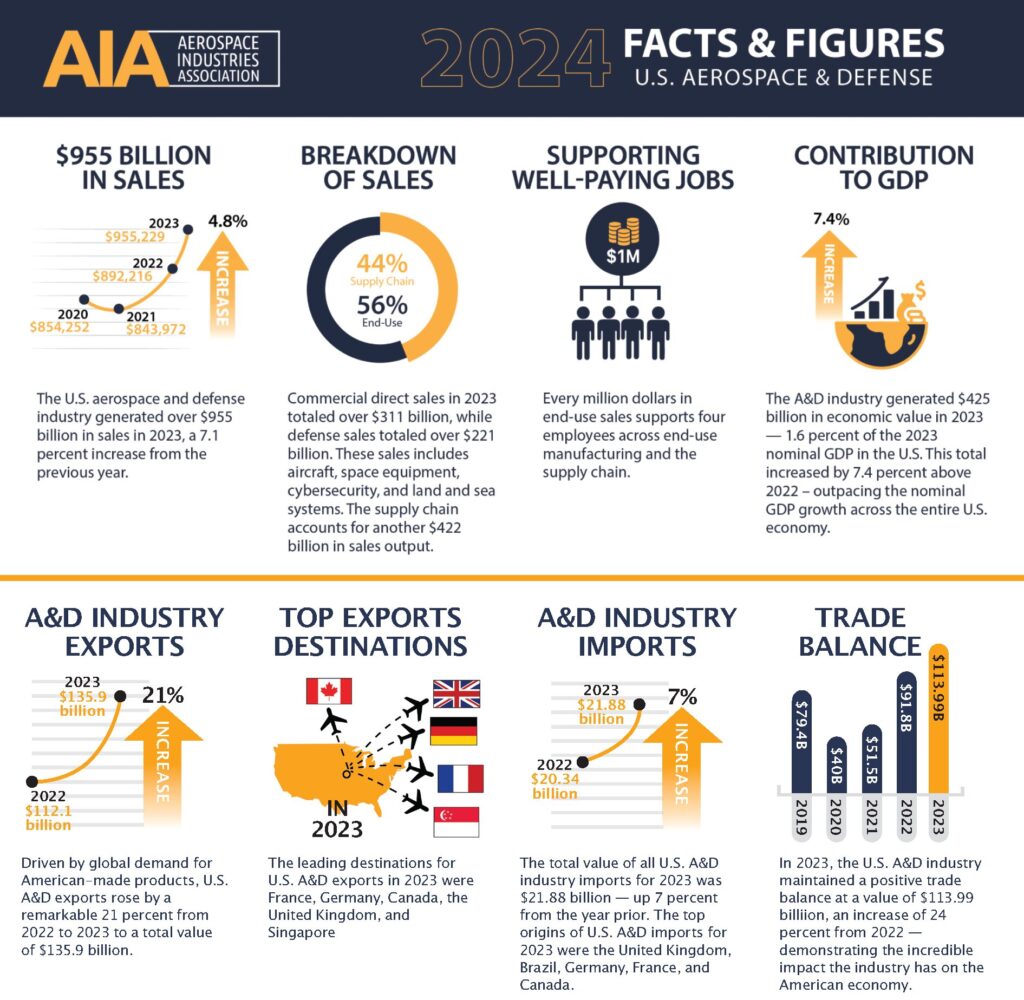

Just how significant is the aerospace and defense industry to the U.S. and states’ economies? Very. It generated more than $955 billion in sales in 2023, according to 2024 Facts & Figures analysis released in September by the Aerospace Industries Association (AIA) in collaboration with S&P Global Market Intelligence. That’s a 7.1% increase over 2022 sales.

The industry generated $455 billion in economic value nationally, or 1.6% of the nominal GDP. According to the data, the top five states for aerospace and defense related economic value are California at $70.4 billion, Washington ($55.2 billion), Texas ($40.7 billion), Arizona ($34.1 billion) and Connecticut ($25.1 billion).

“This year’s Facts and Figures shows that the American aerospace and defense industry continues to be an economic powerhouse — outpacing national averages for job creation and wages and contributing significantly to global trade, national security and technology leadership,” said Eric Fanning, AIA’s president and CEO, announcing the 2023 numbers. “We take pride in maintaining the gold standard in aviation, delivering cutting-edge equipment for modern warfighters, and enabling international collaboration with our allies and partners. With our world-class workforce, advanced supply chain and high-quality innovations, the American aerospace and defense industry stands as one of our country’s strongest strategic assets.”

AIA pegs the industry’s workforce at 2.2 million workers, nearly 60% of whom work in supply-chain functions. Other aerospace and defense workforce statistics from AIA include these:

- The commercial aerospace sector makes up 47% of the industry’s direct employment with the defense and national security sector comprising the remaining 53%. This study divides the A&D industry into four key subsectors, and of those the aeronautics/aircraft is the largest employer, directly employing 462,000 workers. The land and sea systems subsector is the next largest with more than 186,000 workers, followed by the space subsector with 145,000 workers, and the cyber sector with 118,000 employed in 2023.

- Jobs supported by the U.S. A&D industry represent 1.4% of the nation’s total employment base.

- The average labor income per job within the A&D industry (both producers of end-use goods and services as well as the supply chain) amounted to $112,000, approximately 50% above the national average — reflecting the highly skilled nature of the workforce.

- A total of $248 billion in labor income supported by the A&D industry represented nearly 2% of the nation’s total labor income.

As for 2024, aerospace and defense companies have been investing in new and expanded facilities across the U.S. and the world. Some recent examples:

In July, GE Aerospace said it will more than $1 billion over five years to increase capacity at its Maintenance, Repair and Overhaul (MRO) and component-repair facilities worldwide. A major part of the MRO funding this year, according to the company, went to construction of a new Services Technology Acceleration Center (STAC) near Cincinnati, Ohio, that opened in September. Its MRO facilities around the world are seeing investment already, in large part to expand support for CFM LEAP aircraft engines. CFM is a joint venture between GE Aerospace and Safran Aircraft Engines.

At the Farnborough Air Show in July, Collins Aerospace, a division of RTX, announced plans to invest $250 million to relocate a manufacturing plant currently in Bedok, Singapore, to a new facility in the country’s Selatar Aerospace Park 15 miles away. The company says construction will begin in the fourth quarter of 2025 and should commence operations in 2028. Collins has had a presence in Singapore since 1975. The company also is investing $200 million to expand its carbon brake production facility in Spokane, Washington. The 70,000-sq.-ft. addition will double production capacity and add about 80 new jobs. (See p. 156 for an interview with Collins’ general manager at the facility.)

Pratt & Whitney, also an RTX business, opened its new 845,000-sq.-ft. facility in Oklahoma City, Oklahoma, where it supports customers of its military aircraft engines, solidifying its position as the business’s largest military engines field location. The $255 million investment will create about 100 jobs, adding to the 500 full-time jobs already at the complex.

“This expansion more than doubles our footprint in Oklahoma City, ensuring we have the capacity and agility to support increased workloads as military programs ramp up and new ones come online,” said Greg Treacy, vice president of Pratt & Whitney in Oklahoma City, at the October opening.

Honeywell is investing $84 million to expand its Olathe, Kansas, manufacturing facility. The 560,000-sq.-ft. facility makes components for avionics, safety and flight control systems and complex radio frequency systems for traffic collision avoidance, radar altimeters and weather radar. The project will result in about 150 new jobs. “Expanding this facility will enable the development of a strong and resilient domestic supply chain for next-generation avionics and printed circuit board assemblies that our commercial and military customers can rely on,” said Jim Currier, president and CEO, Honeywell Aerospace Technologies, in a statement.

GKN Aerospace completed an 80,000-sq.-ft. expansion at its facility in Chihuahua, Mexico, one of three it operates in the country. Workers at the factory assemble composite aerostructures and manufacture electrical wiring interconnection systems. “By diversifying the site,” says the company, “with the addition of electrical wiring systems capability alongside its existing aerostructures capabilities, Chihuahua will be repositioned as a multi-technology aerospace manufacturing center with the creation of more than 200 new jobs.” GKN Aerospace also plans to increase the capacity and efficiency of its manufacturing facility in Trollhättan, Sweden.

For some insights into what’s driving today’s aerospace and defense industry location decisions, Site Selection turned to some experts at JLL who work with the industry to find the best sites. Following are their takes on navigating the A&D location landscape.

How are site location factors for aerospace and defense projects evolving? In other words, are certain criteria more important now than in the past, such as access to specialized labor or supplies of rare earth minerals?

Tom Taylor, Managing Director, Aerospace and Defense, JLL Work Dynamics:

The industry is experiencing growing demand for products and services. This growth is characterized by more and varied industry demands such as remote defense and space applications. Today the industry is faced with greater demand for faster development cycles, extreme adoption and integration of digital/AI systems across all solutions and products, and more sophisticated and flexible supply chains to ensure delivery of materials and components to de-risk production requirements.

Aerospace & Defense, JLL Work Dynamics

To meet these demands, location footprints and site selection are moving beyond the industries’ tried and true legacy markets to identify markets that can meet the unique operating needs of the enterprise and provide a competitive advantage for these evolving industry demands.

There are several criteria that would be considered important for a new location investment, and three of those are highlighted as follows:

First, labor has always been an important location criterion, but with the rising demand for digital/AI and advanced technologies it is becoming a more critical consideration in A&D site selection initiatives for engineering and development processes. The advanced skills are in high demand across all industries, so A&D enterprises finding a market they can successfully recruit in and creating a strong value proposition for drawing new candidates is critical.

For production operations, sourcing skilled labor is a growing business concern. A recent National Association of Manufacturers survey noted that three out of four U.S. manufacturers noted talent as their primary business challenge. The increased priority for production talent is [due to] insufficient trade or tech school output to meet growing manufacturing activity, turnover in the A&D industry and an aging workforce moving into retirement.

Second, cost is a growing priority as margins have been affected by inflation, supply-chain disruption and workforce challenges. While gaining access to talent to drive innovation will still place operations in higher-cost markets, companies are seeking to diversify their location footprints to achieve labor and supply-chain cost savings. State and local incentives are an element of the cost-conscious criterion. Incentives can play a large role in offsetting start-up costs and provide an ongoing income stream to lower operating costs and preserve margins.

Third, real estate availability can be a critical criterion for specialized or large-scale operations. For example, space vehicle testing, or land-based launch systems could require real estate sites with specific attributes that are not easily found. Factors associated with noise control, proximity to residential, schools and sensitive businesses are all highly considered for these site locations.

What makes a location (state or metro) competitive today as A&D companies consider site options?

Scott Redabaugh, Managing Director, Location Consulting, JLL:

States and communities with a robust workforce development ecosystem will have a distinct advantage in pursuing A&D location investments. States should have innovative recruitment and training solutions that accelerate a new operation’s start-up. For new start-ups and established operations needing new skills, the workforce solution should be fully customized to each company’s unique talent needs, processes and culture.

“States and communities with a robust workforce development ecosystem will have a distinct advantage in pursuing A&D location investments.”

— Scott Redabaugh, Managing Director, Location Consulting, JLL

A regional partnership across technical colleges, trade associations and even high schools can be an asset in developing a workforce pipeline for production operations while advancing new production technologies and processes to meet continual innovation of operations.

The final, key element of the workforce development ecosystem is the depth of university output in critical disciplines like engineering, computer science, AI/machine learning and data science. To help regions best compete, the institutions must fully embrace collaboration and partnership with industry to adapt and customize coursework and degree programs to the needs of industry. This will include undergraduate, graduate and continuing education offerings.

Incentives can play an important role for the competitiveness of a state or community. Incentives are valuable for organizations seeking to ensure long-term access to talent, improve speed to market and minimize investment costs and tax burden. Examples of incentives that may benefit an A&D organization include infrastructure grants for site improvements, tax reduction (inventory, property, sales, corporate income), tax credits, payroll tax rebates and electricity cost reduction.