Chinese Inward FDI Has Slowed But Still Flows

Released in July 2024 by the Department of Foreign Investment Administration of China’s Ministry of Commerce (MOFCOM), the “Statistical Bulletin of FDI in China 2024” analyzes FDI by industry and sector, by region and by source, including analysis of FDI performance and global FDI as well as appendices to show data changes over the years.

Realized value of 2023 FDI into China fell by 13.7%, the largest decrease in growth rate since a 13.2% drop-off in 2009 and one of only three instances of negative movement since 2000. However, the total dollar amount of more than $163.2 billion still represented more than 12% of all global realized value of FDI, good enough to rank second in the world and No. 1 among developing countries for the 32nd consecutive year.

The share of business revenue (20.4%) and share of profit (23.4%) by industrial foreign invested enterprises (FIEs) above a designated size were the lowest in 20 years, but still relatively healthy at $3.7 trillion and $247.3 billion, respectively.

Analysis from Bain & Company’s biennial operations survey of CEOs and COOs released in November shows a rise of more than 25% in the proportion of companies seeking to reduce dependence on China. “The proportion of companies reporting moves to shift operations out of China,” Bain said in a release, “has risen to 69% in 2024, from 55% in 2022.”

Where It’s Going, Where It’s From

As for those still investing there, Guangdong, Shanghai and Zhejiang led by number of newly established FIEs, while Jiangsu, Shanghai and Guangdong (in that order) led by realized FDI value. The Yangtze River Economic Belt (Shanghai, Jiangsu, Zhejiang, Anhui, Jiangxi, Hubei, Hunan, Chongqing, Sichuan, Guizhou and Yunnan) accounted for nearly 51% of all incoming FDI value at more than $83 billion, followed by more than $21 billion poured into the Beijing-Tianjin-Hebei region (good for 13% by value).

A chart tabulating new FIEs from “BRI partner countries” (i.e. the 140-plus countries touched by China’s Belt and Road Initiative) features a startling increase to 13,693 new FIEs in 2023, nearly double the 7,521 new FIEs in 2022. The FIEs from those countries in 2023 represented more than 25% of all new FIEs.

A similar surge is evident in the category of new FIEs from “other BRICS countries,” i.e. South Africa, Iran, Egypt, Ethiopia, and the United Arab Emirates. A total of 1,821 new FIEs came from those nations in 2023, up from 752 in 2022 and 991 in 2021. By realized FDI value, the UAE’s $2.2 billion (from 72 new FIEs) places the country 10th in 2023, just behind the $3.3 billion from the United States and its 1,920 new FIEs.

Moreover, even as companies move some of their previous Chinese operations to ASEAN countries — Brunei Darussalam, Burma, Cambodia, Indonesia, Laos, Malaysia, Philippines, Singapore, Thailand and Vietnam — FIES from ASEAN are coming to China: 2023 saw 2,887 enterprises from ASEAN investing in China, the highest total ever and more than 1,000 more than the 1,833 tallied in 2022. (With $63 billion in overall global outward FDI in 2023, Singapore had the second-highest growth rate in that category at 20.6%, trailing only France’s 37.1%.) In 2023, MOFCOM says, Asian countries (regions) accounted for 76.8% of the newly established FIEs in China, and 81.3% of the total realized FDI (albeit while counting the massive amounts from Chinese territories Hong Kong and Macao as foreign investment due to those jurisdictions’ separate legal and economic status).

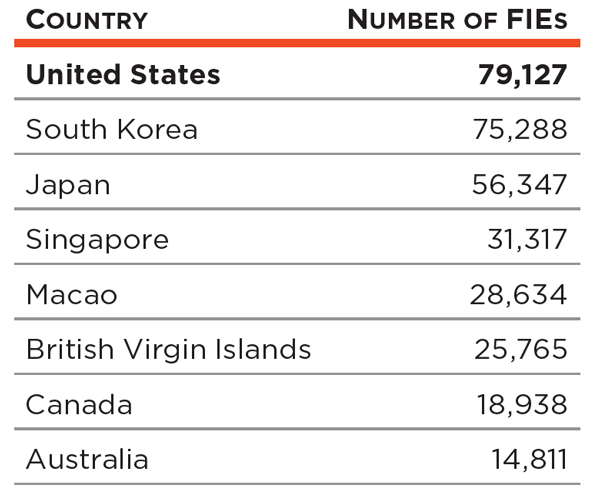

By individual nation, the 546,335 cumulative FIEs from Hong Kong top the totals, followed by 137,771 FIEs from Taiwan (which MOFCOM calls a “province of China”). Here’s how the rest of the top 10 nations play out:

Germany (12,704) and the United Kingdom (12,404) are next in line.

FDI by sector in 2023 was led in terms of realized FDI value by manufacturing ($45.5 billion), scientific research and technology services ($29.4 billion) and leasing and business services ($26.4 billion). By number of new FIEs, wholesale and retailing tops the list with 18,010.

Vietnam Gets Attention

As the rest of the world is seeing the value of Mexico and Vietnam as destinations, Chinese firms are too.

As the rest of the world is seeing the value of Mexico and Vietnam as destinations, Chinese firms are too.

According to an August 2024 report from the International Monetary Fund, “in 2022–23 the number of China’s outward FDI projects declined substantially for many European and Asian AEs, while total flows to non-aligned ‘connector’ countries — most notably Mexico, Vietnam — have more than doubled … Specifically, China’s announced FDI to Vietnam and Mexico in 2022–23 relative to 2018–19 was about 170 and 300%,” equivalent to 2% and 0.5% of these countries’ GDP respectively.”

Vietnam is one of three Asian nations (along with India and Malaysia) getting votes for “most ripe for new investment” in the Site Selection Site Selectors Survey elsewhere in this issue. One of the industries booming there is plastics. A December release from the Plastics Industry Association notes that Vietnam has surpassed South Korea and Taiwan to become the fourth largest plastics import source in the U.S. plastic products market, with imports from the country totaling $2.3 billion in 2023.

An East West Associates survey of 150 manufacturers with operations in China asked where they were looking to relocate (with multiple responses allowed). Asia was the top choice at 74%, followed by Mexico at 53% and the United States at 37%. In a webinar, East West Associates consultants noted that the existing supplier network, engineering support and product design in China are stronger than stretched capabilities in Mexico. “When you are sourcing for some sub-assembly, in China they’d go to suppliers who could figure it out for you,” said Jacob Miller. “In Mexico, you might have to help that supplier find sub-components and other suppliers. So it can become a bigger project than you’d expect in China, where you could just send drawings for sub-assembly.”

“If you think for the long term you’re going to be wedded to a group of suppliers in China, going to Southeast Asia is better than moving to Mexico,” added his colleague Dan McLeod, owing to lower labor costs and the availability of significant and transparent incentives from countries such as Vietnam and Thailand. Moreover, Miller noted, things “might be easier to do in Southeast Asia because there are a lot of factories in Vietnam and Thailand that are not running at full capacity. In Mexico, they’re at full capacity already and convincing them to expand capacity or take on a new project can be difficult.”