Data on data centers might require a data center.

As an adjunct to Site Selection’s July 2026 “Data Centers and Local Labor Markets” industry report by contributors Dany Bahar and Greg Wright, we present here a grab bag of insights that are flooding our inbox at nearly the same pace as the data center announcements themselves. — Ed.

Resonating with Site Selection’s findings that Texas leads all states in data center projects and project-affiliated job creation since January 2024, Cushman & Wakefield’s 2026 Global Data Center Market Comparison report named Dallas the No. 1 primary data center market in the world, followed by Atlanta (2), Virginia (3), Columbus (4) and Johor, Malaysia (5). “Austin-San Antonio and West Texas led the secondary and tertiary market rankings, underscoring Texas’ growing importance as a large-scale AI infrastructure hub,” the firm announced in May. The report analyzes 107 global markets across 24 variables tied to commercial real estate fundamentals, power infrastructure, development activity, regulation and operational risk.

Graphics courtesy of Cushman & Wakefield

Virginia remains the world’s largest data center market with 11.3 gigawatts (GW) of operational capacity. Global capacity under construction approached 31.7 GW in 2025, “more than doubling from 12.5 GW reported in the prior edition of the report,” Cushman & Wakefield stated. Meanwhile, planned capacity across the Americas increased more than fourfold year-over-year, rising from 46.1 GW in 2024 to 191.3 GW by the end of 2025.

Globally, average power delivery timelines for new large-load requests now stand at 4.4 years, with timelines extending to approximately five years across both the Americas and EMEA. “As a result, developers are increasingly pursuing powered land opportunities, integrating private generation into projects and expanding into secondary and tertiary markets where infrastructure constraints may be less severe,” the report said.

“The industry’s focus has shifted from simply securing land to securing deliverable power,” said Cushman & Wakefield Head of Data Center Insights John McWilliams. “That dynamic is fundamentally reshaping data center real estate strategy worldwide.”

Released at nearly the same time as the Cushman & Wakefield report, the new Data Center Readiness Index from AI-services and regulatory intelligence platform Labrynth (creator of the Red Tape Index) ranked Texas No. 1, followed by Oregon, Illinois, Florida and Georgia.

“The rankings suggest that future AI infrastructure growth may increasingly shift toward states capable of combining power availability, operational certainty, workforce depth and infrastructure scalability rather than relying solely on legacy data center concentration,” said Stuart Lacey, founder and CEO of Labrynth. “For years, every state has told its own story about how ready it is. The Data Center Readiness Index puts all 50 states on the same map, scored across the same dimensions using transparent public data. It’s a productivity tool. When everyone is working from the same evidence, capital moves faster, projects break ground sooner and infrastructure decisions become easier to compare across markets.”

Top 10 States in the 2026 Data Center Readiness Index

- Texas

- Oregon

- Illinois

- Florida

- Georgia

- Ohio

- Maryland

- Connecticut

- Massachusetts

- Virginia

The index is free of charge and available to the public.

Newmark’s 2026 Data Center Market Outlook blends analysis of data centers into a larger context involving other industrial sectors. “Spending on data center construction is now up nearly 400% since 2020,” the report states. “That drastic escalation in build-out requires a supply chain and thus is significantly boosting demand for core industrial real estate – warehouses, industrial outdoor storage, manufacturing facilities. This is especially apparent in markets with a Powered Industries Ecosystem — where digital infrastructure, power generation, advanced manufacturing and secure supply chain growth converge to supercharge industrial real estate demand. The measure of that halo effect is one of the biggest questions top of mind for industrial real estate investors.”

Focusing on Texas as the country’s most dynamic powered industries ecosystem, Newmark’s analysis of statewide industrial real estate occupancy and leasing trends found the following:

- Texas is home to 337 existing data centers, with almost another quarter of current inventory under construction. Existing data centers in Texas generate an average of 531,000 sq. ft. of “supportive industrial occupancy — reinforcing Texas’ deep strengths as a supply chain, energy, and manufacturing powerhouse — a true powered industries ecosystem.”

- Data-center-related industrial leasing grew to nearly 14 million sq. ft. in 2025, more than double five years ago.

- “Current data center projects in the Texas pipeline could generate more than 24 million sq. ft. of additional industrial space needs statewide, with proposed projects adding another 14 million sq. ft.

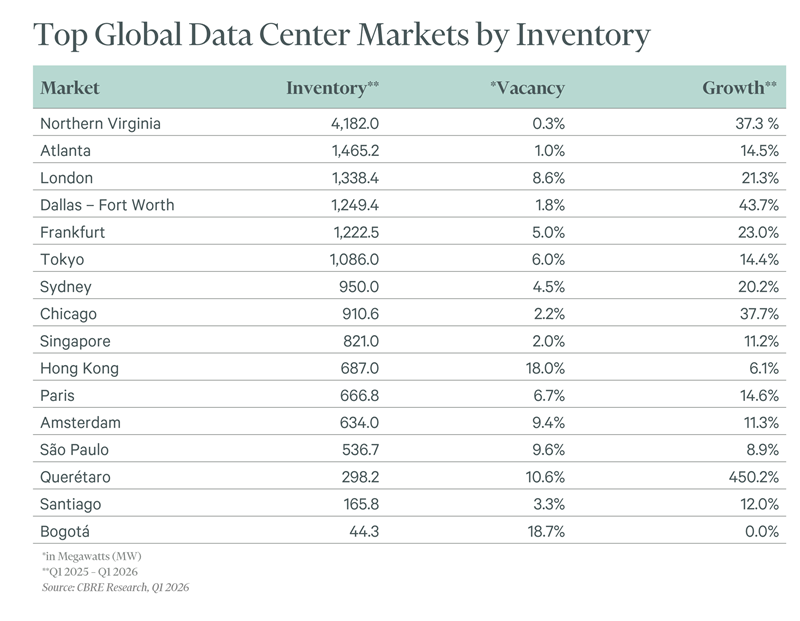

Released in June, CBRE’s Global Data Center Trends report found that global supply reached 16 GW in Q1 2026 across the 16 largest data center markets, up 25% over the past year. But average vacancy fell to 6.7% from 8.3% a year earlier.

“Across the globe, demand is outpacing even aggressive new supply increases, which means companies can no longer assume capacity will be available when they need it,” said Pat Lynch, executive managing director, CBRE Data Center Solutions. “Occupiers are having to secure space earlier, take what’s available from a capacity standpoint and prioritize markets with dependable power to support long-term growth.”

“Northern Virginia, Atlanta, Dallas-Fort Worth and Chicago anchor U.S. growth, collectively adding 1,950.8 megawatts (MW) of new space since Q1 2025 — a 33% gain that marks the fourth consecutive year of double-digit percentage growth,” CBRE stated. “This new supply has been quickly absorbed, pushing vacancy to extremely low levels, including 0.3% in Northern Virginia and 1.8% in Dallas-Fort Worth. Strong leasing activity from large AI rollouts drove record absorption (2,236.2 MW), up 34% year over year.

“Similar supply-demand dynamics are unfolding globally,” the report continued. “In Latin America, inventory across São Paulo; Bogotá; Querétaro, Mexico; and Santiago, Chile increased by 41% over the past year to 1,045 MW, yet strong demand from large cloud and AI users is quickly absorbing new space. In Europe, demand increased by 90% compared with Q1 2025 levels, led by Frankfurt and London, further tightening already constrained markets. Across Asia-Pacific, availability declined by nearly half over the past year to 248.4 MW, with large blocks of space increasingly difficult to secure in markets such as Singapore.”

Photo courtesy of ORNL, U.S. Dept. of Energy

Research continues on new ways to manage data center cooling. Shown here is a wide view of the Central Energy plant that powers the Oak Ridge National Laboratory supercomputer called Frontier. “In this space, waste heat is extracted from circulating water that also supplies room-temperature water to the data center,” says ORNL. “One of the innovations that makes Frontier so energy efficient is this ‘warm-water’ cooling system.”

Amid developments such as the new moratorium in New York, new analysis from Good Jobs First, “Even Cloudier with a Greater Loss of Spending Control: How Data Center Tax Abatements Undermine Public Budgets,” reveals that the four states already known to be losing more than $1 billion annually to data center tax exemptions have all reported significantly higher costs since the organization’s first report in April 2025. “Transparency also remains an issue,” said GJF, noting that “14 states with data center tax exemptions still do not publish comprehensive annual revenue-loss figures, making it difficult for lawmakers and taxpayers to understand the true cost of the incentives.”

But those incentives are out there. Montrose Group reported in June that, according to the National Conference of State Legislatures, “38 states now offer dedicated data center tax incentives, up from 36 in 2024. Kansas became the 37th state to enact incentives in mid-2025. Most programs center on sales and use tax exemptions for data center equipment, power infrastructure and, in some states, energy costs. Texas, Virginia, and Illinois lead in total subsidy volume. Ohio’s program offered a sales tax abatement for data centers investing at least $100 million and meeting an annual payroll threshold, which let the state compete aggressively across the Midwest and Southeast. Meanwhile, the 12 states without dedicated legislation risk falling behind.”

And now for something completely different.

Wood Mackenzie in June issued a report on the next data center frontier: space. “The next generation of AI agents could consume between 10,000 and 40,000 times more computing power per task than today’s chatbots. That pressure is pushing some of the world’s largest technology companies to consider putting their data centers in space,” the firm stated. There’s just one problem: A hypothetical 1-GW orbital data center will set you back around $170 billion — more than three times the cost of an equivalent terrestrial facility, thanks to launch and satellite costs. But those costs might come down.

“Global orbital launch attempts reached 324 in 2025, a 25% increase over 2024, with commercial operators conducting 70% of those attempts,” the report stated. “Launch costs have already fallen approximately 90% with current-generation reusable rockets compared to their expendable predecessors. A record 4,517 satellites were deployed into orbit in 2025, 58% more than the previous year, with 87% owned by private entities.

“SpaceX and xAI have announced ambitious plans to put 100 GW of orbital computing capacity into space annually, a figure 10 times the combined announced pipeline of every other orbital data center developer in the world,” the report continued. “Non-U.S. companies account for less than 0.5 GW of total planned orbital capacity, reflecting how concentrated this emerging sector is among U.S.-based firms. Despite the higher costs, launch activities across the top five companies are expected to begin accelerating between 2027 and 2028.”

“We forecast US$9 trillion of terrestrial data center investment between now and 2040,” said Robert Liew, research director at Wood Mackenzie. “That is where capital goes first. Orbital data centres are a serious long-term proposition, but right now they remain a bet on the cost curve.”

See Site Selection’s May 2026 report on Mexico-based KIO Data Centers’ extraterrestrial plans.