A conversation with JLL’s Sean Farney.

Day after day, hour by hour, second by digital second, the data centers keep coming.

Market research firm Dell’Oro Group in February said the multi-year AI expansion cycle is projected to drive worldwide data center capex to $1.7 trillion by 2030. But even as economic development leaders, elected officials and utilities celebrate project wins, they’re also issuing new ultimatums. Some world regions have declared moratoriums.

All of which makes it a perfect time to check in with the data center experts at JLL, which in January released its 2026 Global Data Center Outlook. The report projects that global data center capacity will nearly double from 103 GW to 200 GW by 2030, requiring up to $3 trillion in total investment over the next five years, including $1.2 trillion in real estate asset value creation and approximately $870 billion in new debt financing, marking “an infrastructure investment supercycle.”

What follows is a Q&A with JLL Vice President, Data Center Strategy Sean Farney.

Site Selection: In the report, your colleague Andy Cvengros observes that “speed to power in 2027 for new developments has become the primary criteria driving site selection as traditional location and cost factors take a back seat to energy availability.”

Sean Farney: Site selection has been converted to a location of power game. It used to be more multi-factor and based on network connectivity to the grid and access to water. But today, given the size of data center developments, power is really factors 1, 2 and 3. Location, location, location is now power, power and power. The areas, regions and localities where data center development is happening today is really based on location of power and large chunks of power in particular.

Major utilities in recent months have come out with forceful statements about making data center customers pay for hogging so much power. Is it your sense that the data center companies understand and accept the pushback?

Sean Farney: Data center companies understand concerns about power bills going up because, as usually the largest consumer of power on the grid, they have the same concerns. They are driven by power efficiency and power cost. They don’t like their bills to increase either. The reality is data centers have absolutely nothing to do with power rates increasing; this is a complex problem centering around outdated grid infrastructure. We as a country kicked the proverbial can on grid updates for decades, and it’s now manifesting in inconvenient and expensive ways. Unfortunately, that has translated into higher bills not only for residential customers but commercial customers, including data centers.

Your report states, “Notably, this outlook presumes that innovations will mitigate persistent energy challenges.” In which locations has your team observed the most impactful energy innovation?

Sean Farney: Traditional utility-based grid connected power generation is done in a bunch of different ways on the back end using wind, solar, coal, natural gas or another form. What we’ve seen happen in the industry recently is this tremendous wave of innovation where private industry hyperscalers have realized that there are power constraints and that the grid does not move fast enough to accommodate their requests to create data centers, which are the result of demand from consumers. The answer is natural gas.

Our culture today is built upon data, which has become the currency of the 21st century. Everyone is reliant upon their devices, and that creates massive amounts of data. In fact, this data increases every year. JLL says that the rate of data creation is about a 24% figure; every four years or so, the amount of data on the earth doubles because of streaming, photos, social media posts and other things that require data centers in the back end to support. Our tech-infused culture is driving this adoption, and it’s even increasing.

So, the way that the data center companies have reacted is in a very innovative way. Instead of pausing data center development and not answering this voracious demand from our tech-infused culture, they’ve spent the time and money researching new alternatives for creation of electrons. This is ushering in a new wave of data center development where new data center developments are attached to the grid and have grid power and/or have bring-your-own-power capabilities.

To what degree are hyperscalers and data center developers enthused about small modular reactors (SMRs) yet also potentially concerned about federal removal of regulatory restrictions on nuclear power development?

Sean Farney: The industry by and large embraces nuclear power and cannot wait for the widespread application of SMRs to power data centers. This will solve all kinds of problems, namely power constraints. SMRs are the greatest lowest impact solution. It’s scalable and consistent, so it will allow almost unlimited data center development from a power perspective. Today, there’s a tremendously high regulatory burden, which slows down the development of nuclear for private use. Actions by the current administration — specifically the Action Plan for America — look to reduce the regulatory burden to speed this technology to market. That’s a great thing for the data center industry, for sustainability and our country in pursuit of maintaining our lead in digital infrastructure. None of the hyperscaler or other data center companies I’ve talked to have any concern about removal of regulatory restrictions. They look forward to it and are partnering as much as possible to pursue this.

One example is the use of the U.S. strategic stockpile of nuclear fuel. If this access is granted, this could optimistically shave a couple of years off the implementation and bring the production date of SMR nuclear forward significantly. That’s something we’re all looking for and it would remove some of the constraints we have today with basic data center developments and sourcing power, whether that’s traditional grid or even gas transmission lines. The ability to bring a 300-MW SMR with you to any piece of dirt really enables fast track development of data centers.

Your report says annual sales of modular systems and micro data centers will reach $48 billion by 2030 as a way around long construction and equipment delivery delays. Can you point to particular modular/micro companies excelling in this arena?

Sean Farney: The industry has advanced modular construction significantly in the last 20 years. JLL has a strategic relationship with a company called InfraPartners, which is a developer of modular solutions where AI-dense infrastructure can be deployed in significantly less time. Other industry leaders, namely Schneider Electric and Vertiv, also have solutions. There are all kinds of good news and great products out there to do this, and they just allow assembly in parallel with site development. This gets you to revenue faster, which is becoming a more important variable.

We’re seeing a keen interest in modular as we start to see AI inference — meaning where trained AI models make predictions or generate outputs from new data inputs as opposed to the training phase where models learn from data — deploy into the enterprise. For technical reasons, one may need to do inference where AI is monetized, on-site, in a retrofitted enterprise data center with a modular solution, or even out in the parking lot. This dramatically reduces the time between deciding to implement AI capabilities and generating revenue from those capabilities.

Your report notes the need, especially in sensitive sectors, for on-prem facilities. How are corporate clients evaluating their on-prem needs today?

Sean Farney: The enterprise has been moving to the cloud and taking a cloud-first strategy for all the right reasons for the last 15 years or so, emptying out on-premises corporate data centers. What they leave behind, which is now valuable, is stranded power. Some of these corporate data centers will have megawatts of power that’s not being used, which is perfect timing as we move into AI inferencing, which every single company in the world will need because if they don’t, their competitor will. Inferencing can be done in a relatively small space — like cabinets. We see 1 MW of deployed gear in five, six or seven cabinets, and that’s a very small space. A corporate data center has enough space to deploy AI; they would only need some retrofitting for power densification and liquid cooling, and they could quickly get to an AI inferencing test dev small production environment in these on-prem facilities. So, it’s a kind of circular strategy but a sustainable strategy for bringing this new technology on.

Your three-phase outline of the AI inference evolution (including regional inference hubs) suggests positive location consequences for regions with plenty of fiber and significant smart city applications and technology.

Sean Farney: The perfect site would have both power and good network connectivity. Dense urban areas can be a challenge if looking at a modular deployment. You would need some space, a parking lot or green space to deploy modules. Some of these dense, smart city-looking type of locations may not be more appropriate versus 20 to 30 miles outside of an NFL city where there’s good fiber and all the other data center site selection variables. From a use case perspective, the AI inference will most likely be deployed close to corporate headquarters or where the engineers are working on the AI inferencing.

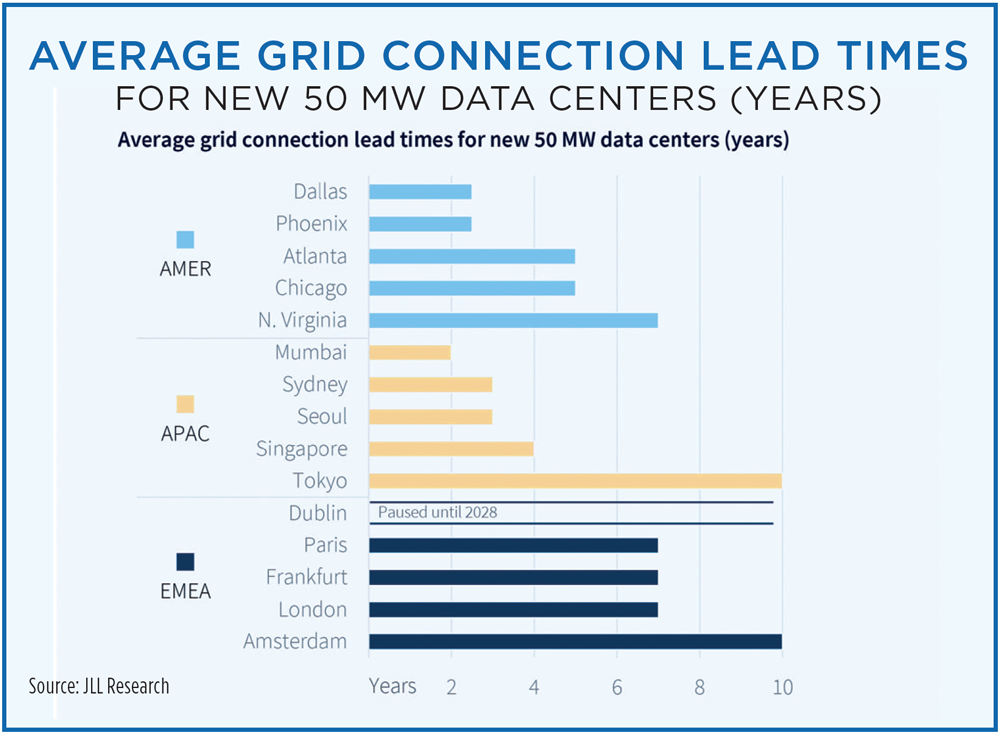

Mumbai displays the shortest grid connection lead time (two years) of the major markets listed in your chart. Does this imply the grid in that region and in India in general is ready for major data center investment?

Sean Farney: India was a data center desert for many years despite its massive population, highly educated workforce and position between major business clusters. A handful of years ago, Microsoft and Amazon both built out cloud availability zones there, and since then, we’ve seen all kinds of data center activity and building. We’ll continue to see uptake and build-outs in the space.