Think Site Selection and you think of the corporate dvecision-maker’s perspective. Think Cresa and you think pure-play tenant representation, i.e. the globe’s leading commercial real estate advisory firm that exclusively represents occupiers. Here, by special arrangement withCresa Head of Research Craig Van Pelt (see Q&A, p. 42), we present excerpts of the newly released Cresa Logistics Index, which examines the top 100 U.S. industrial markets by warehouse/industrial inventory through the lens of being either tenant or landlord favorable. Indexed across market rent, occupancy and building metrics, the report’s top 20 markets by overall tenant favorability are featured below, along with top tenant-favorable markets across the three metrics categories. —Ed.

The purpose of the Cresa Logistics Index is to provide a snapshot of broad market conditions and to compare these to other markets. Fast-growing markets with oversupply and rising availabilities are the most tenant favorable. Several different categories were evaluated and ranked from 1 through 100 based on whether it was considered tenant favorable or landlord favorable.

Efforts to level the components of the index were utilized to remove the overall size of a market compared to others, such as evaluating a change in a market criterion as a percentage of total current inventory. This allows for comparison of large markets such as Chicago with smaller markets like Birmingham, Alabama. These categories were further divided into larger groups: 1) Market Rent Metrics, 2) Occupancy Metrics, and 3) Building Metrics. Data points were collected from seven separate categories:

- Market rent percentage change (quarter-over-quarter)

- Market rent percentage change (1-year)

- Total vacancy rate (current)

- Availability rate (current)

- Sublease square footage as a percentage of inventory (current)

- Net delivered square footage as a percentage of inventory (1-year)

- Under construction as a percentage of inventory (current).

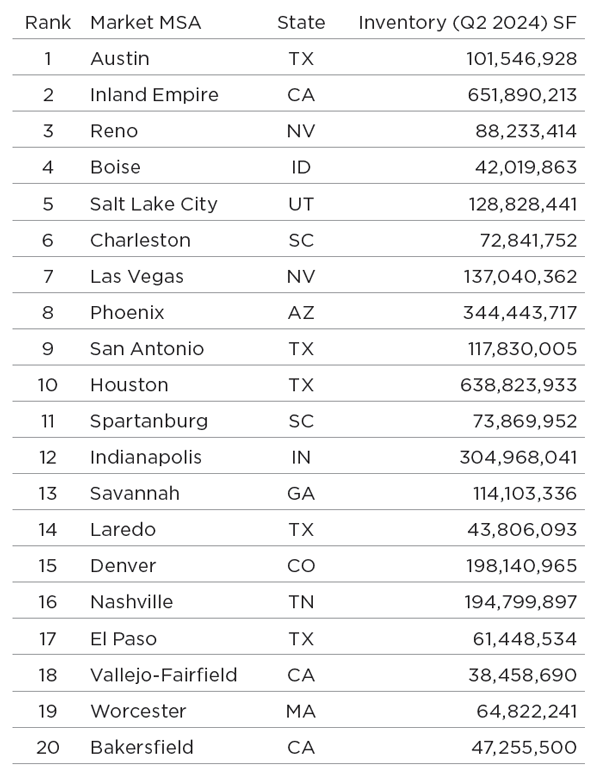

Among the criteria for the index: Industrial logistics space (warehouse/ distribution), buildings over 50,000 sq. ft., Class A & B, non-owner occupied. The top 100 markets in terms of total square feeet were included in the index. The data was collected from CoStar and Cresa data points.

The Charts

Markets with high levels of new construction and high vacancies and availabilities are considered the most tenant favorable. The Austin and Inland Empire markets, despite several years of strong growth, are waiting for demand to catch up to supply, triggering landlords to be motivated to make concessions to close deals.

Without further ado, here are the top 20 markets by tenant favorability:

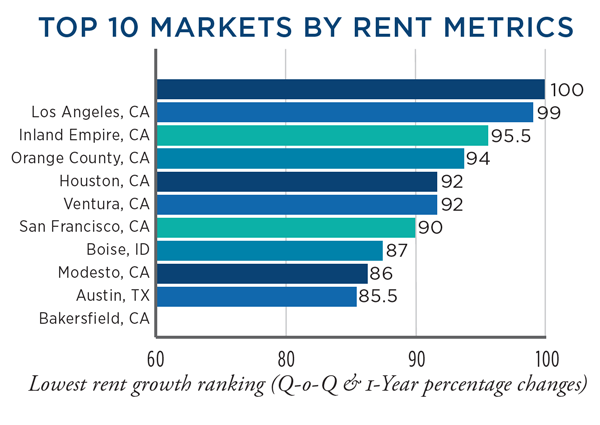

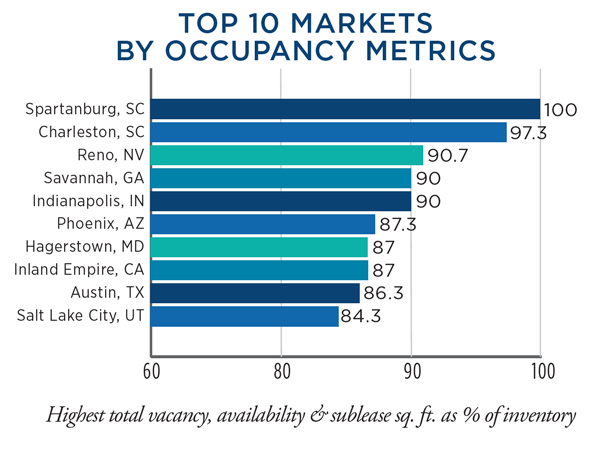

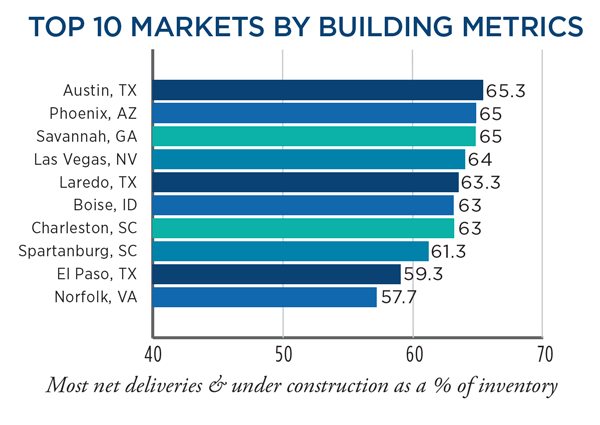

Here are the top 10 across three different metrics categories:

Several southern California markets were ranked tenant favorable due to falling rents. The Inland Empire experienced double-digit yearly rent increases in both 2021 and 2022. After years of sharp increases and a robust construction pipeline, rents have retreated, dropping more than 10% year over year, providing a window for tenants. Other fast-growing industrial markets like Houston and Austin rank tenant favorable.

Markets with oversupply have led to increased availabilities and spiking sublease square footage. These markets include several fast-growing markets, including Spartanburg, South Carolina, which recorded a 25.3% availability rate last quarter, ranking the highest in terms of occupancy metrics.

Source: Cresa Logistics Index

The markets noted as tenant favorable due to building metrics included high amounts of new construction as part of the historic levels of new supply under construction and delivered in the past several years. Austin and Phoenix both had over 10% of their total inventory delivered in the past year.

Three Questions for Craig Van PelT

Cresa’s Head of Research responded to three questions from Site Selection about the Cresa Logistics Index findings.

A number of markets Site Selection has recently identified as attractors of corporate end-user project investment are also in the Cresa Logistics Index Top 10 Most Tenant Favorable, with your No. 1 Austin ranked last spring as our No. 1 Top Metro by Projects Per Capita. It seems counter-intuitive that such a hot market would be the most tenant favorable. How do you explain the dynamics in such dynamic areas as Austin, Phoenix and others?

Craig Van Pelt,

Head of Research, Cresa

Craig Van Pelt: Yes, it is counter-intuitive, but these markets are somewhat a victim of their own success, and the window of tenant favorable circumstances may likely be short-lived. The demand has spurred historic levels of construction, particularly spec construction. A slowdown in demand due to elevated inflation and general economic headwinds has resulted in oversupply. This has caused rents to slow down and, in some cases, retreat as vacancies rise. With recently completed construction awaiting tenants, landlords are more willing to negotiate terms.

One question your index prompts is how fast certain growing markets’ boundaries and definitions are changing. Which locations among the index’s most tenant favorable markets stand out to you in this regard?

Van Pelt: The fastest-growing markets are coupled with quickly expanding populations that can provide the labor to maintain growth. Markets like Phoenix, Las Vegas and Austin can easily expand because there are not natural boundaries to slow growth. This has made the barriers to entry low because there is the ability to find available land. However, the rising cost of construction and higher interest rates have pushed rates higher, which may slow growth in the mid-term.

It seems that some markets identified as the most landlord favorable can still be relative bargains for tenants looking to diversify or grow their logistics footprints. Which stand out to you?

Van Pelt: That’s a good point because, while there has not been the same type of construction levels within landlord favorable markets, stability has not caused the same type of rent escalations that have been seen in other markets. It should also be noted that many of the tenant favorable markets are considered smaller or mid-sized. In particular, the most landlord favorable market in the index — Hickory, North Carolina — has seen moderate increases in asking rates, but is still well-below the national average. Hickory is also well-located from a distribution standpoint and is shifting away from traditional manufacturing like textiles to an important factor in modern internet infrastructure as a key maker of fiber-optic cable. The result will likely be an increase in demand for logistics centers. Other more traditional markets that served as important manufacturers in the steel and automotive industry — like Toledo, Cleveland, and other similar markets — have low vacancy rates but competitive asking rates. With reshoring trends gaining steam and government incentives sparking investment in manufacturing, these traditional markets are well-positioned for growth. The lower asking rates in these markets are relative bargains compared to other markets.