The Bureau of Labor Statistics’ planned move out of 845,000 sq. ft. at Postal Square in the nation’s capital was originally launched in 2022.

2017 photo by Ray Flores courtesy of U.S. Department of Labor and Defense Visual Information Distribution Service (DVIDS)

As DOGE depositions make the social media rounds this week, DOGE-driven dispositions remain a long-term topic in real estate circles.

The volume of federal building space due to come on the market after the federal workforce purge by the Department of Government Efficiency was a major factor behind global commercial real estate advisor Avison Young’s creation of the Federal Property Pulse, a go-to-resource for market intelligence designed to analyze federal leases and their impacts on markets across the U.S.

When launched last June, some of the key findings included:

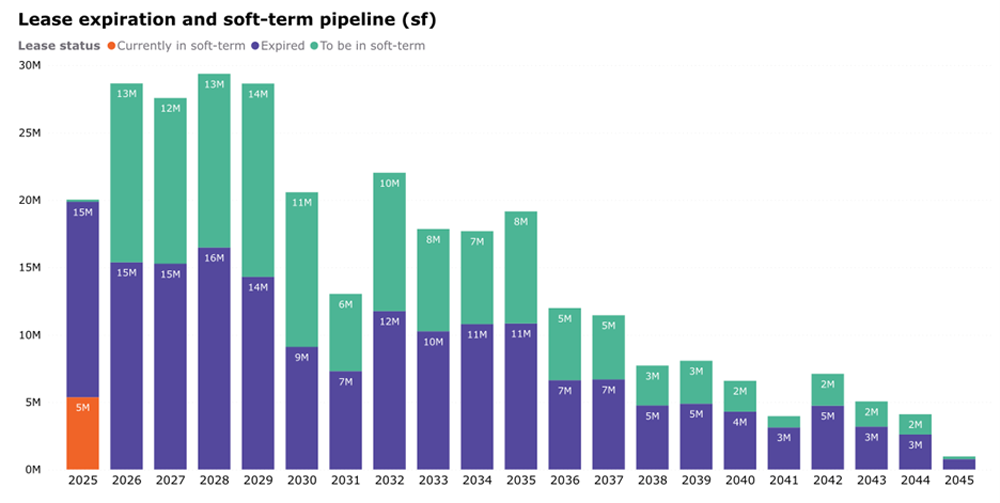

- Over 90% of canceled General Services Administration (GSA) leases were either in “soft-term”, “holdover” or approaching soft-term in 2025.

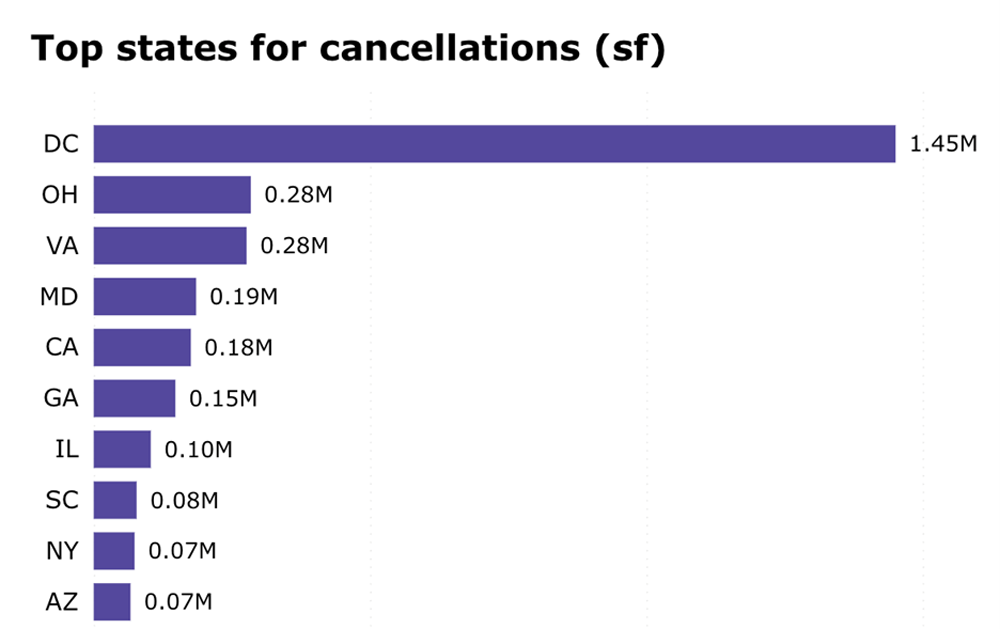

- Nearly 6 million sq. ft. of GSA leases had been terminated, representing a 3.4% reduction in the federal government’s leased space nationwide, with the Bureau of Labor Statistics experiencing the largest cancellation of square footage with more than 845,000 sq. ft. withdrawn from a single lease, while the Fish and Wildlife Service saw the highest number of lease cancellations – 33 in total – amounting to approximately 260,000 sq. ft. (A larger BLS space consolidation initiative was launched years ago prior to the current administration. — Ed.)

A soft-term lease “refers to a government lease where the initial non-cancellable term has expired, allowing the tenant (typically a federal agency) to terminate the lease with a relatively short notice period, often ranging from 120 to 180 days,” Avison Young stated, noting that soft-term leases are considered riskier for landlords than “firm-term” leases, as the government has the flexibility to vacate or reduce space with limited notice.

Holdover refers to when a “lease has expired, but the government tenant is still occupying the space without a formal renewal or extension in place. This typically results in a month-to-month occupancy where the government is paying upwards of 150% of the base rent prior to expiration,” Avison Young explains. “However, in some cases, the government can leverage its sovereign immunity to maintain current rates or in rare cases forgo rent as a new lease agreement is negotiated.”

As analyzed by the Brookings Institution’s Glencora Haskins and Tracy Hadden Loh earlier this month, the hardest-hit market is the “DMV,” otherwise known as the District of Columbia and its neighboring Maryland and Virginia suburbs, where direct federal government civilian jobs account for nearly 10% of employment (and don’t include private-sector government contracting jobs). But other markets are impacted as well.

Source: Avison Young Federal Property Pulse

I recently spoke with Tucker White, Avison Young’s Boston-based U.S. office lead and U.S. life science lead for market intelligence, and Danny Mangru, Avison Young’s New York-based U.S. office lead, about the creation of the new database and about the challenges and opportunities for corporate occupiers, property owners and communities when it comes to repurposing or redeveloping all that former federal space. White said it was driven by market demand, as investors in the D.C. and Mid-Atlantic market in particular wanted to know how great their risk exposure was.

Danny Mangru, Avison Young

“We would have to go to all these sources and it would just take too long to bring everything. together to give them an appropriate analysis,” White explains. “So we created this tool, leveraging our data science team, which is very tech savvy and can scrape all this information from websites and make an automated process where now we’re tracking this live.”

White describes the first half of 2025 as “relatively busy” in terms of the amount of cuts that were made on the GSA real estate front, as the low-hanging fruit of leases in soft term or holdover were addressed. Activity during the second half of the year was driven in part by legislative measures, including a couple from the Trump administration and the Use It Act instituted by the Biden administration.

“Basically they had to get all their ducks in a row,” White says. “All the federal agencies had to create or adopt technology to understand who’s coming into the office space — just basic utilization analysis that companies use. GSA had applied the same logic and they needed a long enough sample size — six months, so into the second half of 2025 — to understand who’s coming to the office. We now expect some more changes are going to happen because there’s a lot of space that’s unutilized within the federal government. So we expect more cuts to come and we’re tracking all of that.”

What does that mean in terms of the overall office market?

“Long story short, it means a little bit more availability for sure,” White says. “They’re the largest tenant in the United States. However, a lot of it’s commodity office space. It’s not the most desirable. And the nice space that the federal government does have — some really nice class A space in D.C., a couple really cool offices in Manhattan — that’s stuff they’re keeping. So a lot of the cuts that are being made are more in secondary markets and more in that Class B, Class C range. A lot of that could be repositioned, whether it’s just the landlord giving the building a facelift and making it more of a Class A – or Class A building, or converting it to another asset type entirely if it pencils out — residential, hotel, in some cases industrial data centers.

Tucker White, Avison Young

“In the short term it’s going to put a little bit of upward pressure on availability,” White says, “which in some select markets could lower rental rates for corporate occupiers in the U.S. But it’s on a sub-market, case-by-case basis.”

Where he sits in Manhattan, it’s not having that much of an effect, Mangru agrees. But D.C. is another story. “The market is extremely bifurcated,” he says. “As a matter of fact, over the last 20 years, I don’t think the market has ever been this bifurcated.”

Leaving D.C. aside because of its government reliance, if you look at every tier-one or gateway office market, he says, 50%, 60% and even up to 80% of leasing is happening in trophy Class A properties. In Manhattan, he observes, trophy only represents 10% of the market but got almost 60% of the demand last year. In Chicago, most of the leasing is coming in the trophy sector, primarily by law firms, Mangru says. Leasing is down, but the top of the market is outperforming pre-COVID averages. “Pretty much across the U.S., trophy leasing is almost 10% above where it was pre-COVID.”

It reflects the appetite from the majority of private-sector occupiers (including tech firms) for quality, well located space. But it’s not necessarily a growth indicator.

“Yes, tenants are going there to get back to the office and to have the best space to retain and attract employees,” White says, “but in some cases, a lot of tenants are going there because there’s a decrease in square footage. They’re able to pay up the rent and it doesn’t affect their bottom line as much.”

“It’s flight to quality, flight to location, flight to efficiency,” Mangru adds, noting that boutique financial services firms are among the sectors eyeing such moves. “For urban locations like Chicago and Manhattan, and to a certain degree like Boston, you could literally move two blocks away and you’re in brand new construction. Yeah, your base rent’s a little bit higher, but you’re probably cutting 20% to 30%. So your overall real estate cost is not really increasing as much as you might think moving into some of these newer buildings.”

What does this mean for the older federal office space coming on the market? White says a larger, slower wave of federal lease cancellations will unfold this year and into next year, and that means analysis is needed to understand the feasibility of converting these buildings. If left as commodity office space with no facelift, the rental discount strategy will be prevalent, he says, i.e., come to the cheap seats. “That’s favorable for a lot of companies, whether it’s a startup that can’t go through their burn rate that quickly or a nonprofit corporation that needs to monitor their real estate a little bit more closely. That plays to those sectors, I don’t think you’re going to be getting a lot of top law firms or tech firms of size going to these buildings if they stay as is.”

But there are other avenues to pursue to make commodity office space compete: In addition to offering amenity packages, entranceways and building systems can be upgraded. Many of these buildings have been around for decades. White says the Avison Young data science team is examining which amenities are going to play better than others and what the cost will be.

“Is the juice worth the squeeze in building out that amenity?” he asks. “Will I get more tenants to my building? Those are all things we’re doing on the office side. I can’t speak for the industrial demand or data center, hospitality or multifamily demand if these buildings are converted, but from an office standpoint, we’re definitely going to be taking a look at some of these buildings.”

Source: Avison Young

Meanwhile, Mangru says, the debt market needs to open up for some of these full-scale renovations to take place. “A lot of these buildings are outdated. What we’re starting to see is some of that capital start to loosen up a bit. But it’s still bifurcated. Right now we’re only seeing that access to capital going to institutions, owners and properties that are performing, which is mostly trophy in Class A. In some markets, we’re starting to see some Class B buildings starting to get access to capital. And if that starts to trickle down into a market like D.C., that’s certainly going to help the cause down the road for future demand.”

White and Mangru say savvy owners/developers will be walking through these spaces with tape measures trying to determine if conversion to multifamily, for example, is feasible. A number of such projects are being proposed in northern Virginia right now. But they’ll encounter space with what White calls “your standard ’80s and ’90s type high-cubicle vibe,” with deferred maintenance issues to boot. But, he adds, some of the properties are “perfectly located. So if that agency does leave, whoever that owner is is going to have an opportunity to maybe get a win out of it” by repositioning the building.

“From a locational standpoint, you could end up undercutting the market to a certain degree if it’s well located,” Mangru observes.

“Chances are you won’t have too much debt on it if the most credible tenant’s been leasing from you for 20- or 30-plus years,” White says. “From just a sheer market standpoint, if you’ve been in the same lease since the ’90s or ’80s or 2000, early 2000s and haven’t updated your space, if you’re working with someone like Avison Young or another good brokerage firm, they’re going to show you how strong the concessions are to move elsewhere because landlords are well capitalized and dishing out tenant improvement allowances right now. So you can have a whole space makeover if you just move or threaten to move and then get the TI allowance from your current landlord as leverage.”

“To Tucker’s point, particularly with law firms, you’re actually seeing a lot more renewals and they’re essentially getting brand new space in that same exact building,” Mangru says. “We’ve seen this across multiple markets where there’s a 200,000-square-foot user in that building and they’ve been there for 20 years and they end up renewing for another 10 to 15 years and they’re essentially getting brand new space. The landlord’s building it out, and they’re getting TI on top of that for whatever furnishings they need. Their net effect of rent is pretty much almost the same if you take those into consideration.”

As for office-to-residential conversions, Mangru says Manhattan and the DMV area are leading the way with some fairly large properties in Manhattan undergoing the transition. But some type of office-to-residential conversion activity is either under way or under serious consideration in virtually every gateway market.

“We’ve started to see it in Dallas,” he says, noting that a recent check of the data showed that nearly 4% of inventory was under consideration or actively underway for conversion. In New Jersey, around 10 million sq. ft. are underway or proposed for conversion. But again, physical challenges can’t be ignored: low ceiling heights; HVAC, plumbing and bathrooms per floor.

“That all compounds as you go vertical,” White says. If you can get past the challenges, some opportunities exist because of those buildings’ old age, i.e., the brick and beam look and historical vibe. But “sewage is a big component when actually considering moving to residential,” Mangru says. “Some of these markets are really not equipped for it, particularly if you’re looking more of the suburban part of these markets. Lastly, it comes down to cost basis, Unless it’s going to be heavily discounted, a lot of times it doesn’t make financial sense.”

Could the ubiquitous data center sector make use of some of this federal space? Mangru says it might make sense for select markets, but a 20-story, aging office building is probably not the ideal place to build data centers.

“We’re seeing some office building conversions take place on the peripherals of the northern Virginia submarket, but there’s been a lot of defensive zoning done now,” White says. “A lot of residents have had enough of the data centers. There have been several office knock-downs to convert to data centers because those offices are located on fiber lines. But moving forward, pretty much everything’s been picked over office wise that could be in northern Virginia.”

As for the data itself, White says Avison Young’s Federal Property Pulse is a competitive advantage for the firm, and there are ways to expand its reach.

“Now we’re looking at doing a 2.0 version which is going to include not just all the negative information of leases being canceled, but also new leases being done,” he says. “The GSA still has demand. It’s not all cancellations. And they also have buildings that they’re selling or buying. So we’ll have another iteration of this hopefully in Q2.”