The index used to determine this year’s Global Best to Invest country and metro rankings is itself determined by sets and subsets of data from 12 different sources:

Country rankings methodology: Conway Projects Database (2 years): total projects, investment and job creation; Kearney Global FDI Confidence Index 2026; UN Development Program Hu-man Development Index; IMD World Competitiveness Rankings; OECD inward FDI data; World Intellectual Property Organization Global Innovation Index; DHL Global Connectedness Index 2026

Metro rankings methodology: Conway Projects Database (5 years): total projects; Kearney Glob-al Cities report; Startup Genome Global Startup Ecosystem Report; IMD Smart Cities Index; Mori Memorial Foundation Global Power Cities Index; Startup Blink Startup Ecosystem Report

Here are more granular insights from two of those sources, beginning with the most recent:

Kearney Global FDI Confidence Index 2026

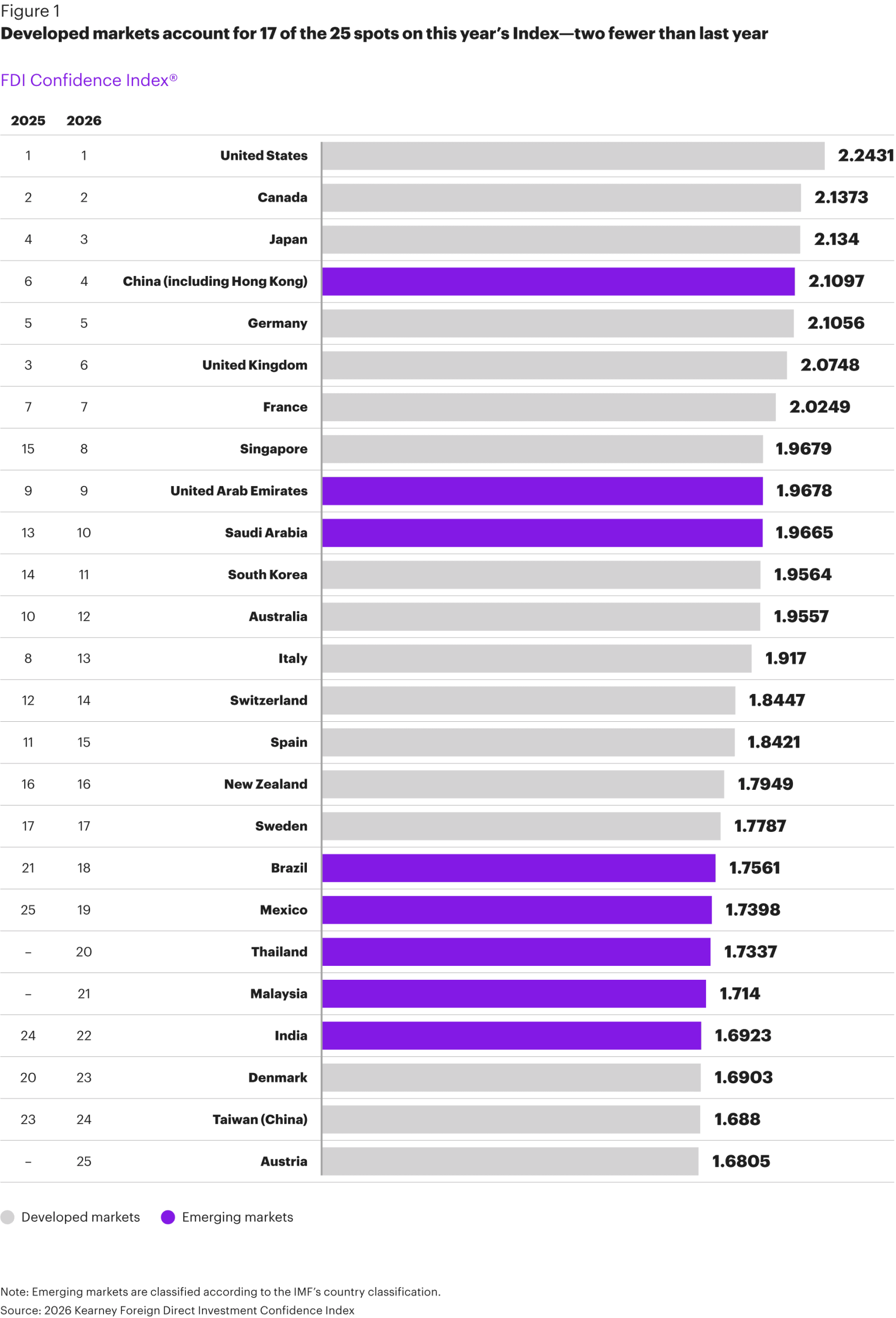

Kearney in April unveiled the findings of its latest FDI Confidence Index, which ranks markets based on their expected attractiveness to investors over the next three years and highlights the factors shaping corporate investment decisions. This year’s edition included a special section examining how investors view the growing role of industrial policy and what it means for corporate investment strategies.

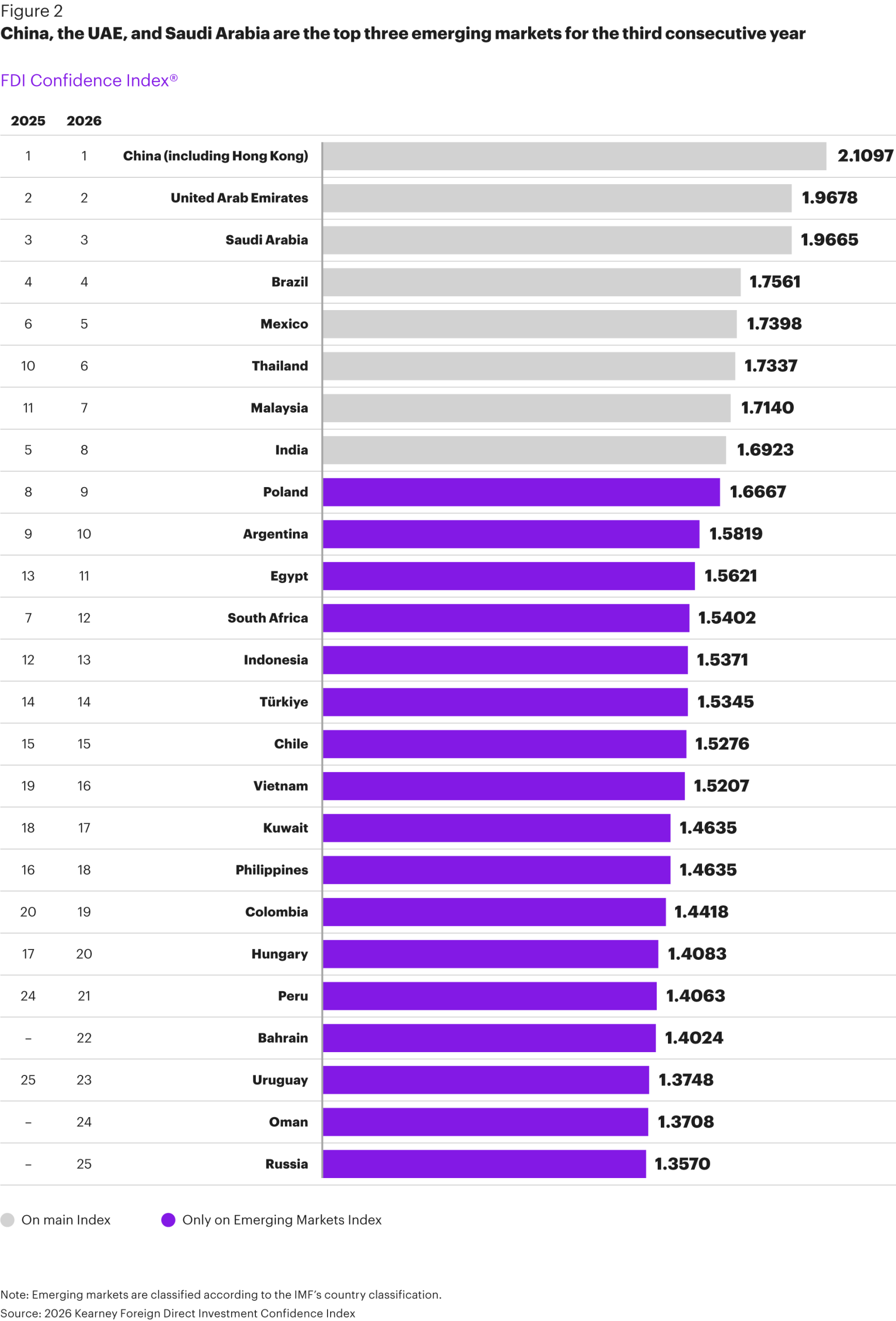

Kearney ranked the United States No. 1 for the 14th straight year, followed by Canada, Japan, China and. Germany, with Site Selection’s No. 1 Global Best to Invest country the United Kingdom at No. 6 after placing third a year ago. The biggest riser among the top 10 was Site Selection’s No. 2 Global Best to Invest metro Singapore (which was our No. 1 last year), rising on Kearney’s index from No. 15 to No. 8. For the first time since 2013, Kearney reported, places in the Asia Pacific claimed the greatest share of the top 25 markets in the index, with 10 in total, and emerging markets (defined as such by the International Monetary Fund) accounted for eight of those top 25.

That trend “suggests investors are evaluating opportunities in a more integrated way, and emerging markets are become more central rather than peripheral in global investment strategies,” said Erik Peterson, Kearney partner and managing director of the Global Business Policy Council, part of Kearney Foresight, during an April 9 web conference on the report’s launch. He made special note of Vietnam’s rise from No. 19 to No. 16 and Peru’s jump from No. 24 to No. 21, calling out Vietnam’s growing role as a hub in Asia’s semiconductor supply chain and the May 2025 launch of a deregulation package in that country.

Among emerging markets, Thailand moves up to No. 6 from No. 10 and Malaysia rises from No. 11 to No. 7, reflecting their growing stature as non-Chinese operations destinations in Asia. What may surprise some is India’s drop from No. 5 to No. 8 among emerging markets, even as it rises from No. 24 to No. 22 in the overall findings encompassing all markets.

“We also see growing momentum among the so-called middle powers,” observed Peterson, calling Singapore the best example, followed by Thailand and Malaysia due to their roles in many companies’ China +1 strategies.

Peterson attributed the U.K.’s drop from third to sixth as potentially related to uncertainty surrounding the nation’s budget at the end of 2025. As for the Americas, net optimism for the coming three years dropped by 17 points in the U.S. while rising by two points in Canada due to that country’s natural resources stability and growing investment in AI and other technologies, Peterson said. Meanwhile, Brazil and Mexico continue to move up in the rankings.

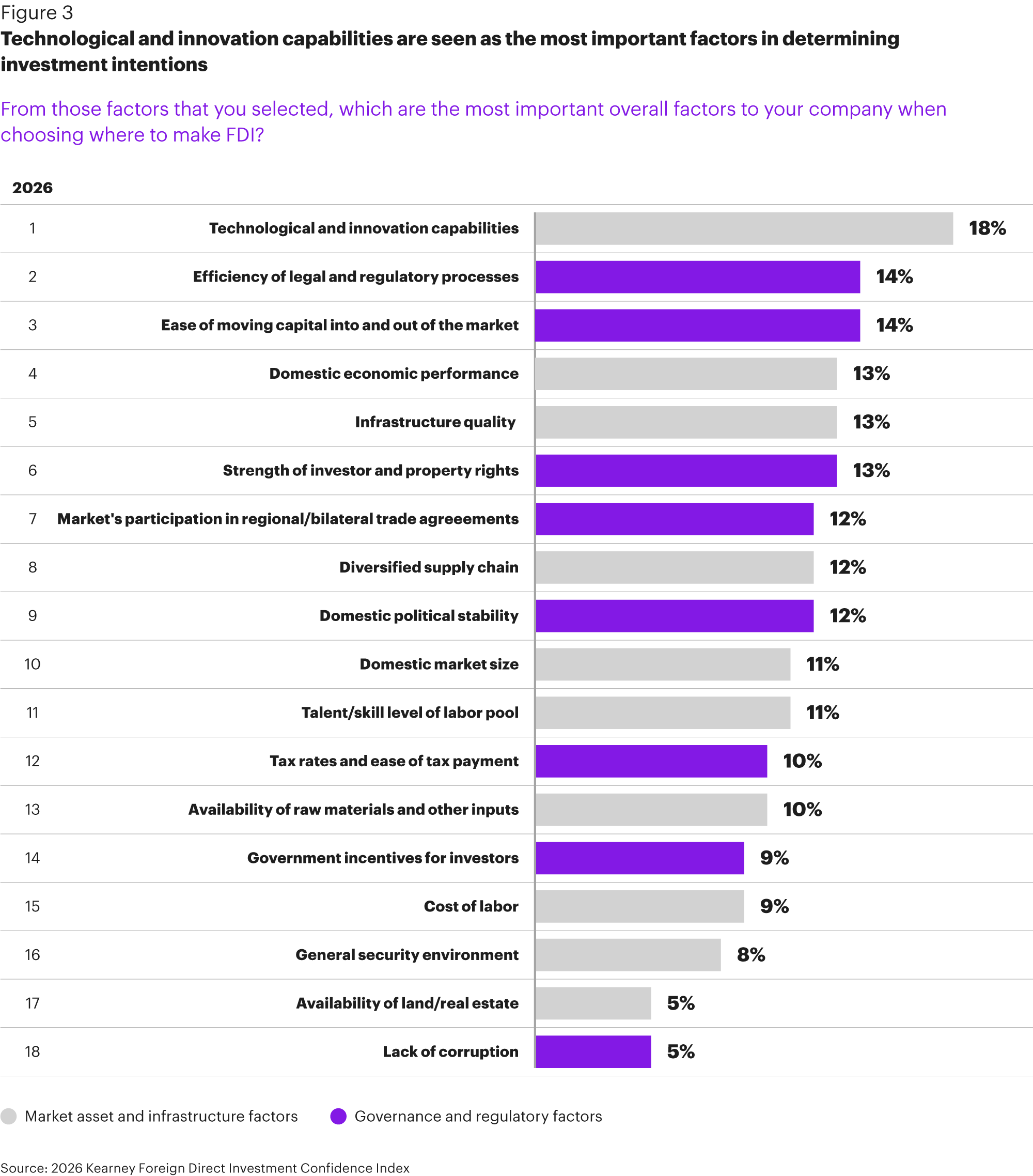

When asked to name the most important overall factors to their companies when choosing where to commit FDI, the No. 1 response was technological and innovation capabilities, which was the strongest reason to invest in 10 of the top 25 markets in the index and reflected investments in a range of technologies — including AI — in several key markets, Peterson said. That was followed by a tie between efficiency of legal and regulatory processes and ease of moving capital into and out of the market. Talent was tied for No. 10 while government incentives tied for No. 12 with cost of labor.

Peterson noted that the survey was conducted prior to the Iran conflict, but “investors even then were anticipating some degree of turbulence in the year ahead,” he said, because of commodity volatility and political instability. Nevertheless, 88% of investors planned to increase their FDI in the next three years.

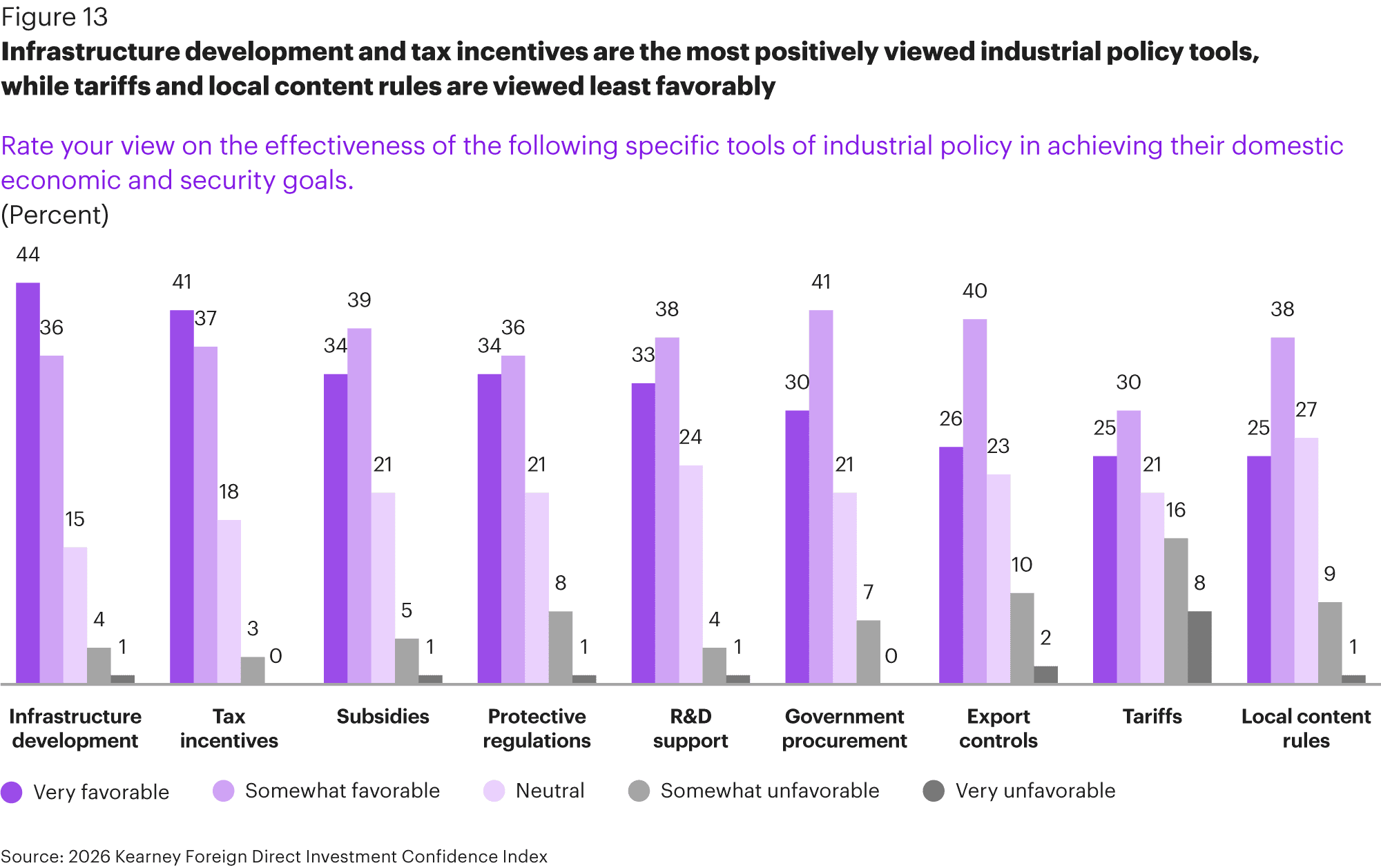

When determining where to direct that FDI, 84% of investors view industrial policy as an extremely important or very important factor, the Kearney survey found. Peterson noted that Kearney’s partners at. Global Trade Alert have documented a 260% rise in global trade policy interventions in various forms such as tariffs, export controls and incentives. Here’s how it breaks down by type of industrial policy respondents viewed as most effective:

Kearney Partner Igor Hulak, stationed in Riyadh, Saudi Arabia, said the practical, consistent and execution-oriented industrial policy of Gulf countries was among the reasons Saudi Arabia and the United Arab Emirates are ranked No. 10 and No. 9, respectively, in this year’s index. The numbers tell the story, he said, with FDI jumping from $20 billion the year before to $45.6 billion in 2024 in the UAE, and $15.7 billion flowing to Saudi Arabia.

Kearney Partner Shirley Santoso from Indonesia remarked that FDI rose by 67% in Thailand in 2025, noting that the country “has done a lot of things to improve the ease of doing business,” decreasing red tape, implementing e-government and one-stop licensing practices and training its labor pool. With lower costs in automotive, electronics and food processing, Thailand has benefited a lot, she said, from China +1 strategies. So has Malaysia, which last year saw a record performance in FDI attraction thanks in large part to its focus on services and high tech, including high-value industries such as electronics and semiconductors.

Santoso also noted that governments and companies alike are intentionally building their talent pipelines across the Asia Pacific region: technical education expansion in Vietnam; promotion of the engineering, IT and digital environment in India; healthcare and English-based services in the Philippines.

DHL Global Connectedness Index

“Globalization remains at a historically high level — despite escalating geopolitical tensions, rising U.S. tariffs and unprecedented uncertainty about future trade policies,” said DHL in March upon the release of the DHL Global Connectedness Report 2026 in partnership with New York University’s Stern School of Business. Based on more than 9 million data points tracking international flows of trade, capital, information and people, the report tracks globalization on a scale from 0% (no cross-border flows) to 100% (borders and distance have no impact). The world’s level of globalization was 25% in 2025, in line with the record high set in 2022, the report found.

“Global trade grew faster in 2025 than in any year since 2017, excluding the volatile Covid-19 period,” stated a summary of the report’s findings. “U.S. importers accelerated shipments early in the year ahead of tariff increases. U.S. imports later dropped below prior-year levels, but rising Chinese exports to non-U.S. markets helped sustain global trade volumes. Trade in AI-related goods surged as countries and companies raced to build AI infrastructure. AI-related products drove 42% of goods trade growth in the first three quarters of 2025, according to WTO figures.”

Among key takeaways from the report:

- U.S.–China trade fell to 2.0% of global trade, down from 2.7% in 2024.

- Singapore is the world’s most globalized nation, followed by Luxembourg and the Netherlands. “Europe is the most globalized region, followed by North America and the Middle East & North Africa. The United Kingdom has the most broadly distributed flows worldwide. The United Arab Emirates recorded the largest increase in globalization since 2001.”

- “One reason trade can keep growing despite U.S. tariff hikes is that most trade does not involve the U.S. In 2025, 13% of imports went to the U.S., and 9% of exports came from the U.S. In addition, many countries are pursuing new trade agreements to secure access to alternative markets.”

- “Multinational firms still earn near-record shares of sales abroad. While announced greenfield foreign direct investment (FDI) fell in 2025, overall FDI flows rose, and cross-border M&A activity remained resilient.”

- Average trade growth through 2029 is expected to be in line with the past decade, expanding by an average of 2.6% per year.

“Globalization is holding its ground — and that alone speaks volumes about its value,” said John Pearson, CEO of DHL Express. “From poverty to climate change, the world’s biggest challenges can only be solved through global thinking. The DHL Global Connectedness Report shows that countries and companies are not retreating behind national borders. That is good news.”

“Even as the U.S. and China decouple, most countries continue to engage with their longstanding partners,” the report found. “Over the past decade, only 4–6% of global goods trade, greenfield FDI and cross-border M&A have shifted away from geopolitical rivals. Of these flows, most have not moved to close allies but to countries with flexible geopolitical positions, such as India and Vietnam. Overall, the world economy remains far from a broad split into rival blocs.”

“The DHL Global Connectedness Report shows that countries and companies are not retreating behind national borders. That is good news.”

— John Pearson, CEO of DHL Express, at a March briefing in Hanoi, Vietnam

“The politics and policy surrounding globalization are much more volatile than the actual flows between countries,” said Prof. Steven A. Altman, director of the DHL Initiative on Globalization at NYU Stern’s Center for the Future of Management. “Global trade patterns changed more in 2025 than they do in a typical year, but less than they did during other recent disruptions such as the early stages of the war in Ukraine. Sound decision-making requires a calibrated view of how much global business ties are really changing. The risks to globalization are real, but so is the resilience of global flows.”