orporate real estate executives like the impact

that Sarbanes-Oxley (SOX) is having on the reporting

|

| Bob Zane |

and management of facility performance. They just wish that compliance

with the law cost less time and money.

That’s the bottom line of a new research study conducted

by the Atlanta-based Industrial Asset Management Council.

“The good news,” said Campbell Soup Real Estate Director Bob Zane, is that the IAMC survey “found corporate real estate can become better positioned to do its job as the function moves toward compliance with the act.”

But the IAMC chairman also said that the survey of

CRE executives revealed some bad news: “the high cost of compliance in

dollars and management time.”

One recent study by RHR International for Directorship

magazine found that large companies are paying an average of US$35 million

a year to comply with the act. Compliance with the law is especially taxing

on small public companies, which have less resources to devote to SOX

audits.

The IAMC survey, sponsored by DADCO Consulting Inc.,

was sent in fall 2004 to corporate real estate and facility management

executives, other managers with real estate responsibilities and top corporate

managers. The survey was closed Nov. 1 with 188 completed responses representing

a broad sampling of industries and company sizes.

About 40 percent of the respondents represented Fortune

500 companies. Manufacturing was the largest sector

|

| Source: “Corporate Real Estate Compliance with the Sarbanes-Oxley Act” Industrial Asset Management Council, February 2005 |

represented (22 percent), followed by financial and insurance institutions

(15 percent), and real estate, rental and leasing companies (11 percent).

The survey attempted to measure executive opinions

on the impact of SOX compliance, particularly Section 404 of Sarbanes-Oxley,

which requires public companies to document and obtain audits of their

internal controls.

SOX was passed by Congress three years ago as an

attempt to clean up the way public companies do business in the wake of

huge accounting scandals at Enron, WorldCom and other large firms.

In 2004, a record number of companies revised their financials in accordance with SOX Section 404. Restatements increased more than 28 percent to a record 414 in 2004 from 323 a year earlier, according to a report by the Huron Consulting Group.

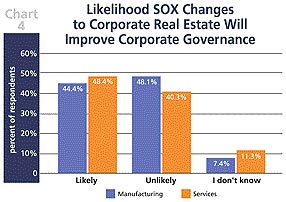

Ironically, most respondents to the IAMC survey said

that the law would not live up to its intent, which was to improve investors’

ability to evaluate the company through its financial statements. Respondents

also felt that real estate department SOX compliance would benefit governance

of large companies but would be less likely to help small firms.

|

Among other findings, the study found that:

- Corporate real estate management (CREM) departments of large companies

and manufacturing firms have already reaped some benefits from SOX

compliance, while small-company CREM departments are much less likely

to see benefits. - Manufacturing company CREM departments are less likely to have

already experienced a SOX audit than service company CREM departments. - Large-company CREM departments spent more time on SOX compliance

in the past six months than small-company CREM departments. However,

both large and small firms anticipate spending less time on SOX compliance

in the next six months than they spent in the past six. - Corporate real estate managers whose departments report through

a business unit are less informed about SOX than corporate real estate

managers whose departments report through corporate finance.

Phil Hammel, director of real estate for Honeywell,

says, “Believe it or not, there is a silver lining to Sarbanes Oxley —

|

| Charles McSwain |

it helps focus the company on the place that real estate occupies within

the financial side of the enterprise.”

Hammel explains that real estate dominates the fixed asset ledger, and only salaries and fringe benefits outweigh facility costs on the profit-and-loss statement. For some companies, getting this sort of attention is the first step toward getting some necessary resources.

“SOX requirements give the real estate director leverage to be provided resources and staffing to make sure that there is a real estate database for starters,” says Hammel, adding that properly scheduled appraisals, operating expense pass-throughs and rent escalations can then receive proper scrutiny.

The prominence of real estate’s role in taking costs

out of a company’s indirect spend is something often heard from CEOs in

media financial reports, says Hammel, which only bodes well.

“That automatically makes real estate important where it counts — the executive suite and the board room,” he says.

CSX’s Charles McSwain, incoming chair of IAMC, says

that “SOX has focused our corporation on the imperative of accountability

at all levels of the corporation. The compliance process has not changed

the reporting process as much as it has driven discipline in conforming

to the process and clarifying each individual’s role and responsibility

in significant transactional work.

“In that sense it’s been good, because most corporations

always want to do the right thing with their shareholders,” he adds. “The

introduction of rules and regulations from the government always becomes

problematic, because there are several

ways to achieve good accountability. But regulation tends to drive one

method over another.”

William Donaldson, chairman of the Securities & Exchange Commission, has said that the real benefit of SOX will come in the long run when greater credibility in the market leads to higher stock prices, but so far corporate managers aren’t convinced.

The key, says McSwain, is to create an accountability process that enables American companies to “compete on a level playing field with their international competitors.” He says the ideal reform would “achieve process improvements that achieve the same results [greater accountability] but improve compliance and reduce costs.”

His peers in the corporate real estate profession would appear to agree.