Exclusive analysis by Cresa explores where law firms are leasing and why.

by Craig Van Pelt, Director and Head of Research, Cresa

Corporations are used to consulting legal counsel as they formulate location strategy. What about when the law firms themselves are the workspace occupiers? Last year, a search by Cresa, the world’s largest commercial real estate tenant advisory, for law firms with a minimum of 5,000 sq. ft. of office space in the United States and Canada identified nearly 13,000 office locations, totaling over 240 million sq. ft. of office space. Moreover, analysis of Inc. 5000 firms by Site Selection last fall found the most dramatic leap upward by percentage in that elite group comes from the legal sector, which added 36 firms to its segment of the Inc. 5000 (a 43% increase) to reach 120 companies and rank No. 15, just behind real estate. Building on work completed in fall 2025, here we present by special arrangement new enterprise research from Cresa Director and Head of Research Craig Van Pelt on one of the only office-occupying sectors that has expanded activity in the past several years. — Ed.

The traditionally conservative legal sector is playing a significant role in the overall recovery of the office market. Although law firms have historically adhered to established practices, the pandemic has accelerated changes in the workplace and the adoption of new technologies. As a result, hybrid working models have become the new standard in the legal sector.

Since the pandemic, overall office leasing volume has dropped by 15% to 20%, and the average lease size has decreased by about 9%. In contrast, the volume of law firm leasing has generally remained steady, with the average lease size increasing by roughly 5%. Larger office leases (over 20,000 sq. ft.) have become increasingly common for law firms. Between 2017 and 2019, law firms made up 4.1% of total office leasing for these larger leases, but this percentage jumped to 5.9% between 2022 and 2025. This change is significant, considering that the total leasing volume for large leases in the past four years has been approximately 715 million sq. ft.

Each firm is unique; many have utilized the current soft office market to right-size their operations by consolidating offices and reducing their overall footprint. However, there are also signs that select firms are beginning to expand their space requirements. There is no “one size fits all” law firm workplace model.

Real estate overhead constitutes a significant investment for firms, typically ranking as the second largest fixed expense and accounting for 4% to 8% of annual gross revenue. As a result, the design of office workplaces is evolving to better align with business strategies, company culture, talent acquisition and the firm’s competitive positioning.

The legal sector has seen a higher rate of employees returning to the office compared to other industries. According to the Kastle Legal Industry Barometer, the occupancy rate for the legal sector on peak days — meaning the days of the week when employees are most present — is about 75% of pre-pandemic levels. In contrast, other office sectors have maintained occupancy rates of around 60% to 65% on peak days. The practice of law heavily relies on building relationships, and in-person meetings, negotiations and client interactions are essential. In a competitive hiring market, law firms utilize their offices as hubs to cultivate company culture and retain employees.

Thinking Beyond Bricks & Mortar

The evolution of real estate strategy from “where we work” to “how we compete” is integrating space decisions with brand, talent, technology and long-term business objectives. High-profile locations (aka flight-to-quality) with hospitality-style amenities and modern meeting facilities reinforce brand identity and prestige. Law firms are considering real estate as a lever — not just a cost. Many firms are exploring smaller footprints, subleasing excess space and considering hub-and-spoke models as part of a more dynamic portfolio approach.

Cloud-based legal tools, secure video conferencing and e-discovery platforms have reduced the need to be physically present in the office daily. Striking a balance between the industry’s traditionally high in-office presence and new expectations for flexibility, rows of private offices, while still prevalent in many law offices, are increasingly giving way to collaborative hubs, with flexible layouts, shared spaces and technology integration that support both client service and attorney development.

The legal sector has seen moderate job growth over the past decade, adding 84,100 jobs, which represents a 7.4% increase. This growth has been slower than that of other office-based jobs, which increased by 14.8% during the same period. While job growth for knowledge workers has been sluggish over the past year, new job postings in legal services have reported an increase of more than 12% year-over-year. However, the legal sector has generally reduced its hiring efforts, leading to many positions remaining unfilled. Additionally, ongoing advancements in AI technology are expected to challenge the industry in the coming decade, prompting a reevaluation of job roles and their impact on real estate.

Law firm footprints have generally remained stable over the years, but there has been a significant change in the amount of square footage allocated per attorney. In the 1990s, law firms typically featured traditional office layouts, which included oversized partner offices, large libraries and considerable file storage. During that time, the average space per attorney ranged from 800 to 1,000 sq. ft. However, many law firms today aim for around 400 to 600 sq. ft. per attorney. This reduction in space is largely due to decreased physical storage requirements and a lower ratio of support staff, leading to more efficient use of office space.

During the 1990s, the average space per attorney ranged from 800 to 1,000 sq. ft. However, many law firms today aim for around 400 to 600 sq. ft. per attorney.

What’s Driving Law Firm Real Estate Decisions

The decision to relocate is complex. Beyond the cost and disruption of moving spaces, firms (especially large Am Law firms, the top 200 law firms ranked in 2025 by highest grossing revenue by The American Lawyer magazine) typically sign long-term lease agreements, making their obligations increasingly significant. Site location decisions are being reshaped by a mix of hybrid work adoption, talent competition, client expectations and cost discipline rather than a wholesale retreat from the office. Both Am Law and non-Am Law firms continue to view physical offices as strategically important, but they are prioritizing high-quality, amenitized buildings.

As firms make decisions about opening or closing offices, relocating or remaining in their current locations, they evaluate key factors to determine how a building or real estate solution can best support their business, financial and operational needs. There are significant variations depending on the type of law practice; however, being close to major clients or industries is crucial for relationship management and business development. Firms often choose locations in financial, corporate or tech hubs based on their specific practice areas. For instance, litigation or corporate law firms may need to be near courts, regulatory agencies or financial centers.

Location decisions will continue to hinge on access to talent, and neighborhoods or submarkets that appeal to attorneys are important factors in the decision-making process. Employees are increasingly seeking amenities that enhance their well-being, such as fitness centers, hospitality-like common areas, nearby restaurants, entertainment options and other features that encourage them to come to the office.

Source: The Am Law 100 & Am Law 200, Law. Com (2025); CoStar, Cresa

Real Estate Brief

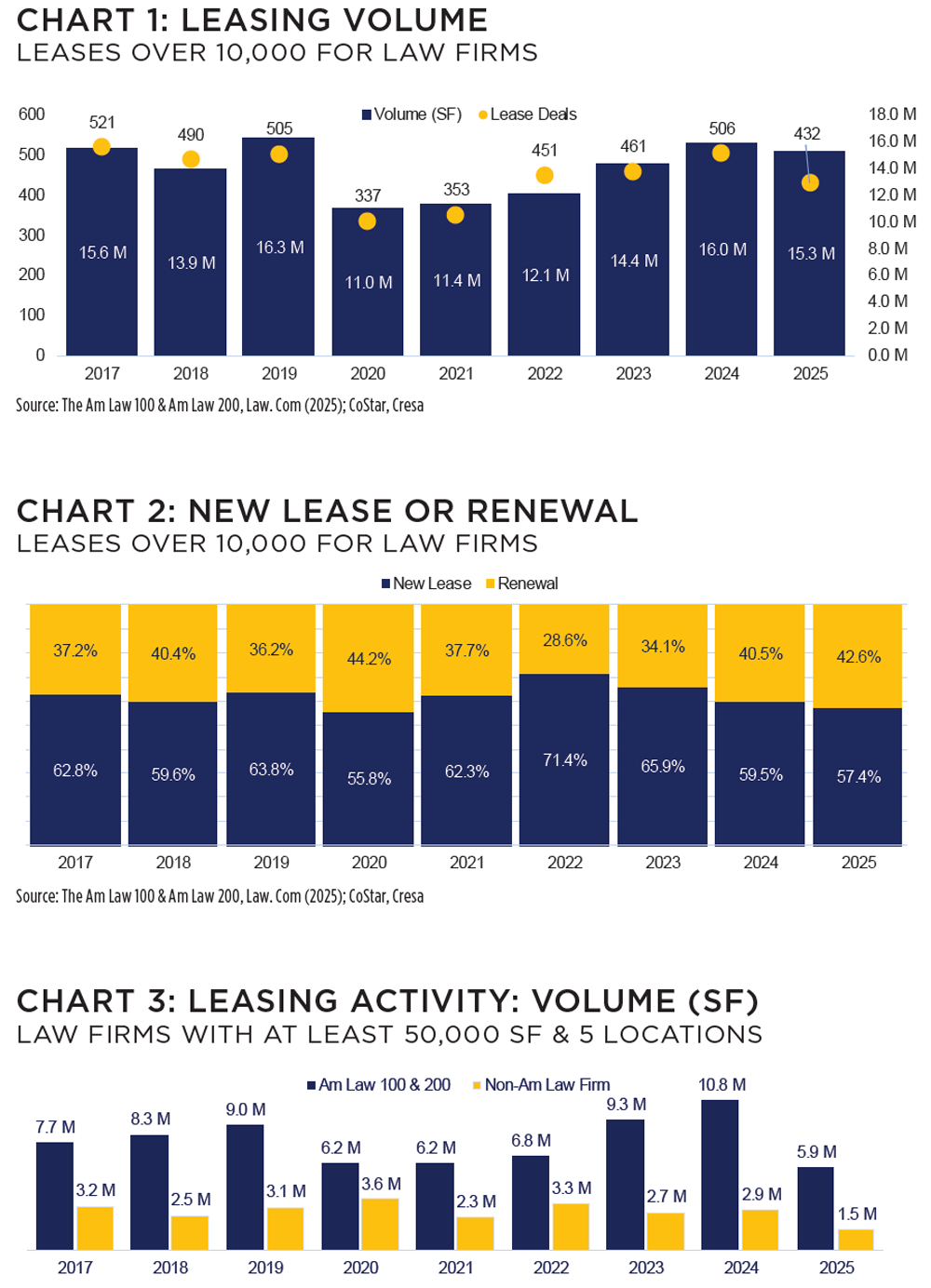

Leasing activity in the legal sector experienced a significant decline from 2020 to 2023. However, in 2023, this activity began to recover and reached a peak in 2024 as the legal sector regained confidence in returning to office protocols and making long-term real estate decisions. (See Chart 1.)

In 2020, during the peak of the pandemic, the percentage of lease renewals increased as law firms became more cautious about their lease decisions. However, in 2022 and 2023, the percentage of new leases surged as law firms capitalized on favorable office market conditions to upgrade or right-size their spaces. As the availability of high-quality, large blocks of office space in top-tier buildings decreased, the number of lease renewals returned to pre-pandemic levels. (See Chart 2.)

The data in Chart 3 encompass transactions from law firms that have at least five office locations and occupy a minimum of 50,000 sq. ft. of total office space. These international, national and regional law firms illustrate broader trends within the legal industry. The data is divided into two categories: Am Law 100 & 200 firms and Non-Am Law firms.

Both Am Law and non-Am Law firms have picked up leasing activity by volume. Based on the activity of law firms of all sizes, larger law firms have been more aggressively completing lease transactions. Am Law firms have historically renewed deals around 30% of the time. During the pandemic, Am Law firms signed a higher percentage of new deals, seizing the opportunity of overall weak office market conditions to relocate and/or right-size their space. It should be noted that new deals may also include signing a “new deal” in the same building for a different size footprint or even on different floors. The percentage of new Am Law deals signed in 2024 fell due to the dwindling of large block availability in newer, highly amenitized buildings.

Burden of Proof

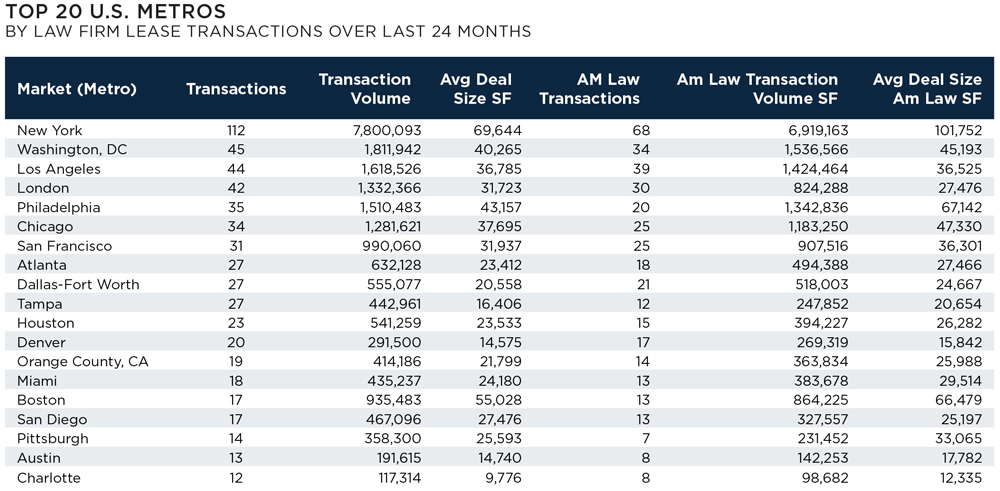

New York and Washington, D.C., are home to more than 75% of Am Law 100 and 200 firms, largely because of their respective proximities to the U.S. financial capital and the federal government. Many firms that have outgrown their current offices are expanding by leasing additional space. For example, Kirkland & Ellis has leased an additional ~130,000 sq. ft. in Manhattan to accommodate its growth beyond its existing headquarters. Similarly, Paul, Weiss signed a significant new lease at 1345 Avenue of the Americas. In Washington, D.C., ArentFox Schiff has announced its relocation of headquarters to consolidate its space from its long-time location on K Street NW.

Other markets have also seen substantial investments from law firms. Chicago and the Midwest remain active with local firms expanding and national firms maintaining significant presences. Major Texas markets, particularly Austin and Dallas, are attracting national and international law firms expanding beyond traditional coastal hubs. On the West Coast, Fisher Phillips has expanded its Los Angeles footprint with new leases in both downtown and Woodland Hills, increasing their square footage.

Source: Cresa analysis of 230+ markets in the U.S., with transactions occurring in 139 of those markets; London included as a comparison point reflecting U.S. firm operations in the UK.

Secondary markets are also gaining attention. Morgan Lewis is relocating its Pittsburgh office to a new building, joining other firms moving to the market. Miller Johnson has doubled its office footprint in Detroit, reflecting growth in the region. Both Am Law and national firms are renewing their commitments or moving to new markets, even in areas with an overall weak office market.

Since the start of 2024, there have been 129 law firm lease transactions over 50,000 sq. ft. Out of those transactions, 73 firms (56.6%) chose to remain in their current buildings, while 49 firms (28.3%) relocated, and seven (5.4%) added another location within the same market. Am Law firms accounted for 76% of the transactions involving spaces over 50,000 sq. ft. and 81% of the total square footage transacted since the beginning of 2024. Of the total transactions, 30 were renewals in place, indicating that these firms did not change their existing footprints. This means that 99 transactions (76.7%) resulted in either an expansion or a contraction of office space.

It is not surprising that many law firms adjusted the size of their spaces, as they typically sign leases ranging from 10 to 20 years, and changes in their space needs occur over such lengthy lease terms. Although there were more expansions than contractions among these 99 transactions, the overall change in size reflected a 5.3% increase. Conversely, the overall office market has seen average lease size decrease between 10 and 15%.

A noticeable trend is emerging toward a “flight to quality,” with organizations increasingly seeking newer, well-amenitized spaces in vibrant neighborhoods. Law firms have also embraced this trend; among the 129 firms needing space over 50,000 sq. ft., 49 chose to relocate. This decision to move is significant, costly and time-consuming, particularly for larger spaces. Among the 49 firms that relocated, 26 expanded their offices, while 23 downsized. Overall, the total space occupied by these 49 law firms increased by 2.8%.

While many firms have changed their office space footprint, it’s important to note that both attorney and staff headcounts have increased. A key metric to consider is the occupancy per attorney at peak levels, with target ratios now set below 500 square ft. per attorney.

As law firms redefine their future, their real estate decisions have become strategic tools for gaining a competitive advantage. They are not just considerations of where and how to work but also reflect adaptations to changing office cultures and evolving client demands. Real estate decisions are complex; what works for one firm may not be suitable for another. Some firms are expanding their office space, while others are choosing to downsize. However, a common theme is that law firms are finding more effective ways to utilize real estate to support both short- and long-term business strategies, create flexible workplace solutions that can adapt over time, and enhance overall operations and productivity.