Light-vehicle production in North America reached 17.2 million units in 2000, plummeting to 8.58 million units in 2009, a result of the Great Recession. After 2009, the footprint of North American production changed, with fewer plants operating more efficiently to reach pre-recession production levels.

Looking ahead, North American light-vehicle production is forecast to increase by 8 percent between 2015 and 2023, from 17.4 million units to 18.9 million units. IHS does not forecast a significant uptick in new plant construction through the close of this decade or early next to support the production increases. Aside from the greenfield investments already announced, the increases in North American vehicle production will be the result of investments into existing facilities designed to increase efficiency and capacity.

According to Joe Langley, production analyst for IHS Automotive, light vehicle production is set to play out differently for the traditional domestic manufacturers (the Detroit Three — General Motors, Fiat Chrysler Automobiles and Ford), compared with production from the foreign-owned transplants (including Daimler AG, BMW, Hyundai, Honda and Toyota, among others).

Production by the transplant automakers is forecast to jump 24 percent, from 8.2 million units in 2015 to 10.2 million in 2023. At the same time, production by the Detroit Three is forecast to fall by 6 percent, from 9.3 million units to 8.7 million units.

I Guess I’ll Have to Go

Regardless of the manufacturer’s home country, however, automakers are shifting production of compact cars to new or existing plants in Mexico. In so doing, automakers are maximizing production of lower-profit-margin vehicles in plants with a lower cost base as well as production of higher-profit-margin trucks and utility vehicles in higher-cost plants in the US and Canada.

Several foreign-owned companies are investing in North American greenfield production sites, with two primary strategies playing out. Some firms are looking to localize production of models for which the US is their primary market, while other investment is driven by product-line expansion that requires new capacity — the latter particularly with German automakers looking to add Mexico production that will service the US and also as an export hub for existing or new vehicles.

Mexico offers lower labor cost, established infrastructure and skilled workforce, as well as extensive free-trade agreements. GM, Ford, FCA, Nissan and Volkswagen have each been producing vehicles in Mexico for decades, and will continue investment into facilities there, as well as into existing US plants. Honda and Mazda both opened new plants in Mexico in 2014, Hyundai (for its subsidiary Kia) is set to start production at an all-new facility in 2016, and BMW’s new Mexico plant is scheduled to see production start in 2019.

In 2017, a new joint-venture plant between Nissan and Daimler AG will begin building Infiniti and Mercedes-Benz products in Aguascalientes, Mexico, specifically for compact cars and utility vehicles. Ford recently announced a new greenfield plant, in San Luis Potosi, set to begin production in 2018, and focusing on C-segment small cars. Volkswagen AG has built a new plant in the country as well, set to begin production of the Audi Q5 in 2016.

Detroit Three Imports

Investment into US and Canada production is focused on product changeovers, with some expansion in the US from transplant automakers adding new products or expanding production capability. While production in Mexico is forecast to increase by 46 percent from 2015 to 2023, US production is expected to increase only 3 percent. Automobile production in Canada is forecast to decline by 30 percent, however, offsetting some of the gains in Mexico.

IHS Automotive forecasts production from the Detroit Three will see year-over-year declines in North America from 2016 to 2023. While automakers are strengthening production of popular (and profitable) utility vehicles and trucks, some programs are delayed. The production footprint is being impacted by a global emphasis on luxury vehicles, and there is expectation for some Detroit Three products to be imported as these companies manage global production footprints.

GM begins importing the Buick Envision from China in mid-2016 and Ford plans to import the next-generation Fiesta, rather than continuing to build the low-margin vehicle in Mexico. Fiat Chrysler Automobiles has announced that it will end production of the Dodge Dart and Chrysler 200 compact and mid-size sedans in the US, converting those plants to production of trucks and utility vehicles.

East and West

The top four Asian manufacturers (Toyota, Honda, Nissan and Hyundai) will grow North American manufacturing footprint by nearly 14 percent collectively, enabled by investment in greenfield plants between 2014 and 2019. Attractions for the investment include the opportunity for global scale, flexibility to adjust production to demand and the opportunity for exports, particularly from Mexico. In some cases, these automakers are reinforcing or expanding production of trucks and utilities, responding to both demand and increasing model flexibility.

These automakers also are shifting their production mix within existing plants. Toyota is adding production of the RAV4 in Canada with the next generation in 2019, while shifting Corolla production to Mexico. Hyundai will use the Mexico facility for C-segment cars, while new investment into its US production will increase production of the Santa Fe utility vehicle, currently in short supply; Hyundai will instead import more Elantra and Sonata sedans from South Korea, offsetting the reduction in US production of those cars.

The North American production footprint has also been positively impacted by investment from the traditional German luxury automakers, with production from Volkswagen, BMW and Daimler forecast to increase through 2023. For these manufacturers, the benefits are in localization, with some production increase a result of portfolio expansion. However, these automakers also have aggressive sales and production targets and risk of over-proliferating their product ranges.

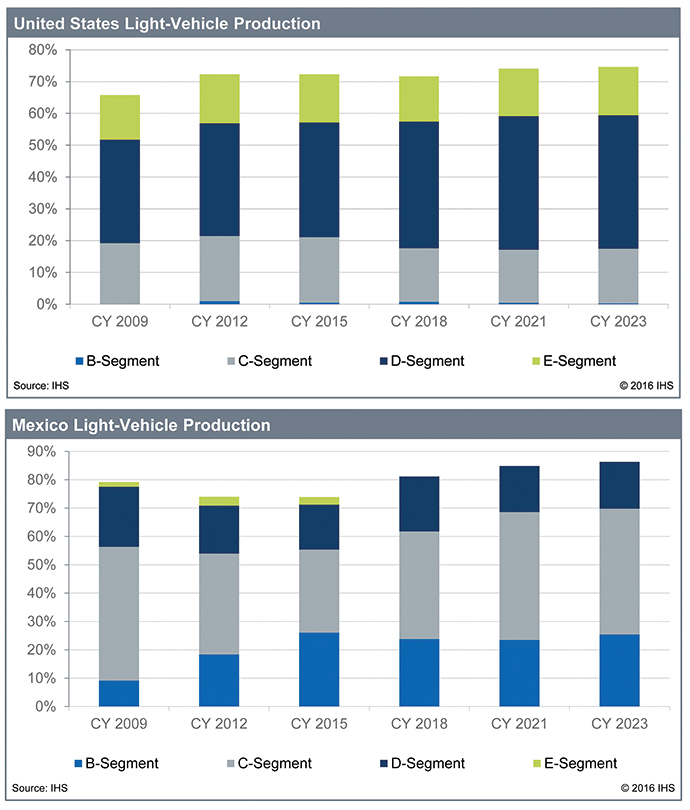

The ABCs of B-C-D

Most North American vehicle production continues to be in the US, which accounts for at least 65 percent of North American production through 2023, followed by Mexico and then Canada. However, the mix of vehicle classes produced in each country is shifting. Production of smaller cars is set to increase as a share of light-vehicle production in Mexico, while decreasing as a share of US light-vehicle production.

Production of subcompact (B-segment) vehicles is growing in Mexico, while accounting for only a fraction of US production and none in Canada. The compact (C-segment) class sees a smaller swing, though production of vehicles in that size is forecast to be a larger portion of production in Mexico, while shrinking as a share of US production. Mid-size vehicles (D-segment) will play a larger role in US production and take a shrinking share of Mexican production.

New plants in Mexico going online between 2014 and 2019 are largely aimed at production of B- and C-segment products, including investments from Mazda, Honda, Toyota, the Daimler/Nissan joint venture, and a new plant for Kia set to begin in production in 2016, as well as the new Ford plant. IHS forecasts the new Ford plant will see C-segment vehicle production, an evolution of the Ford Focus platform, while the Michigan Assembly Plant, which currently produces the Focus, will be repurposed for truck and SUV production. (At press time, Ford announced a $1.4-billion, 500-job investment in its Livonia, Michigan, transmission plant, where it will build a 10-speed rear-wheel-drive transmission.)

Honda has been producing vehicles in Mexico since 1995 at its plant in El Salto, while the Celeya plant opened in 2014 produces the B-segment Fit and related HR-V utility vehicle. Production in the existing El Salto facility is forecast to shift from C-segment CR-V production to HR-V production in 2017, while Honda is also investing $52 million in its plant in Indiana to boost production of the CR-V beginning in 2017, shifting production of the higher-profit-margin vehicle to a higher-cost plant.

Overall, the North American vehicle market is a mature one, as compared to an emerging or high-growth market, both in terms of production and sales. The market maturity is among the reasons why investment frequently focuses on improvement of current facilities, and greenfield investment is expected to be minimal going forward.

Stephanie Brinley is Senior Analyst-Americas, IHS Automotive, covering North and South America for the IHS World Markets Automotive service.