by Pei Wen Ng, Consultant, Tractus (Singapore office)

Expanding into Asia? You are likely grappling with one of the most fundamental questions for growth: Should you build a new facility from the ground up, or acquire an existing operation? Let’s explore how the “build vs. buy” choice can shape investment outcomes and decision-making in the region.

The Choice That Defines Your Entry

The “build vs. buy” question seems straightforward, but the answer rarely is. What might seem to be an operational question about your manufacturing unit’s site selection on the surface, is actually a core strategic question involving your short- and long-term outlook. How do you balance your need for control and customization against the urgent pressure to get to market quickly? The answer rarely lies at either extreme; rather, it depends on a company’s strategic horizon as well as its appetite for risk.

The Build Path: Control and Customization

If you have a long-term vision and “patient capital,” building a new facility (a “greenfield” project) offers unmatched control. You get to design everything from the ground up, from embedding the latest technology and optimizing for sustainability, to hiring management and staff that you prefer and designing/fitting out the shop floor to your exact specifications. Southeast Asian markets such as Singapore, Thailand, Vietnam, Malaysia and Indonesia have sharpened their appeal through generous FDI incentives, ready industrial infrastructure and investor-friendly industrial zones. Under Thailand’s Board of Investment (BOI), for instance, qualifying projects can receive tax holidays, import duty exemptions and land-use flexibility, reducing the effective cost of building. As all these countries compete for FDI, their investment attraction boards all offer different packages to attract investors.

But this control comes at a cost: time. Be prepared for a long journey because greenfield projects typically take 12 to 36 months to be realized. You will also need to navigate a maze of local permits, zoning laws, environmental approvals or other criteria. This path is best for long-term players, like manufacturers or logistics firms, who are building a permanent regional hub and must be close to a mass of existing clients in the region.

A good example is LEGO Group’s $1 billion carbon-neutral plant in Vietnam, which broke ground in 2022 and began operations in 2025. Tractus supported the site evaluation and investment location assessment during the project’s early planning stage. The project demonstrates both the opportunities and the long lead times, about three years from announcement to production, that are typical of large-scale greenfield investments.

Photos courtesy of LEGO Group

The Buy Path: Speed and Instant Access

In fast-moving sectors like health care, consumer tech, e-commerce or retail, speed to market is critical. Here, acquiring an existing business is often the fastest way in. You are not just buying assets; you are in fact buying time. The acquisitions route offers a fast track to market presence, leveraging existing infrastructure, workforce and customer relationships. One of Tractus’ recent advisory and M&A projects involved a Japanese health care company evaluating expansion in Thailand and, in order to rapidly grow their presence in that market, purely focusing on the M&A route. Rather than constructing new facilities, the investor targeted acquisition of established operators with existing production capacity and market licenses. This acquisition-first route provided:

- Immediate market entry: allowing the client to become operational within months, not years.

- Regulatory head start: inheriting local licenses and certifications, such as IP and trademarks which were needed in their line of industry.

- Instant brand trust: acquiring a known brand and its customer relationships, with international distributions contracts in place.

By acquiring an already operational platform, the investor effectively bought time and flexibility to later expand production capacity through new builds once demand validated the market. The challenge here, however, is unearthing and vetting the right kind of acquisition targets who are keen to sell and the potential pitfalls that can occur during the transaction and due diligence process. Common issues include limited target availability, valuation mismatches, incomplete financial documentation and legacy liabilities such as environmental or tax exposures. Cultural integration and post-merger alignment can also slow down synergies if not managed early.

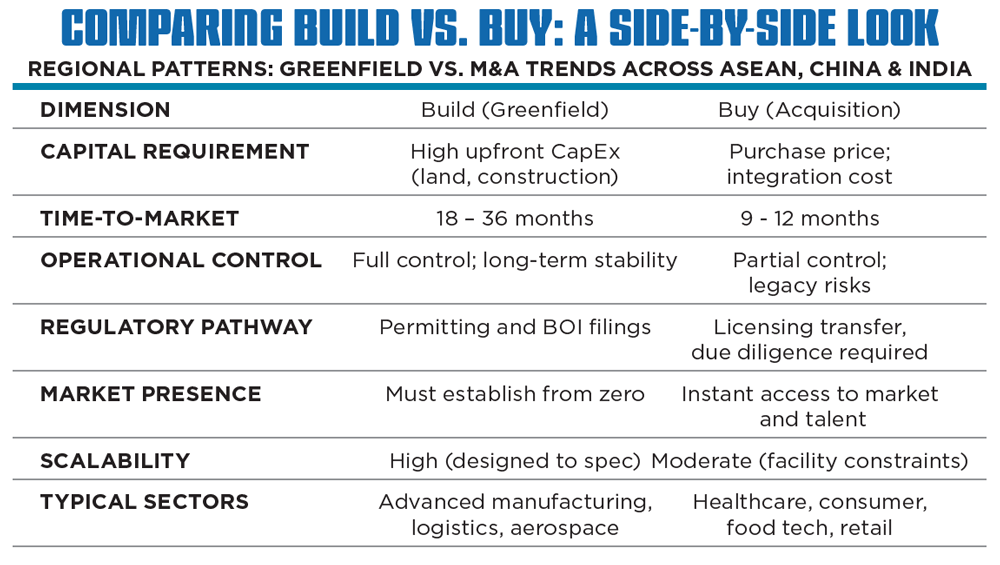

Comparing Build vs. Buy: A Side-by-Side Look

In Southeast Asian markets like Thailand, Malaysia, Singapore and Vietnam, governments have actively created build-friendly ecosystems as they look to aggressively bring in FDI, set up plants and create jobs. With developed industrial zones, the path to constructing a new facility is well-paved. In Thailand’s Eastern Economic Corridor (EEC), companies can co-locate with their supply chain, benefiting from developed automotive and electronics clusters, with streamlined permits and strong infrastructure. Here, the traditional headaches of building from scratch are greatly reduced. Similarly, Malaysia’s MIDA has designated high-tech and green industrial parks such as the Kulim Hi-Tech Park and Penang Science Park, providing plug-and-play infrastructure for electronics and the semiconductor industry.

In Singapore, the Economic Development Board (EDB) continues to advance the nation’s “Manufacturing 2030” vision by offering land-ready industrial estates and innovation hubs in areas such as Tuas Mega Port and Jurong Innovation District.

According to EMIS, PwC and S&P Global, M&A activity across Asia remained resilient in 2024 despite macroeconomic headwinds. This is led by ASEAN with 3,224 deals, reflecting strong mid-market momentum (EMIS). India recorded 646 deals (PwC), supported by domestic demand and policy reforms, while China saw 1,569 deals (S&P Global) amid cautious sentiment and fewer large transactions.

In Asia, 2024 greenfield investments (by value) into ASEAN and India saw a 10% and 28% Y-o-Y growth, respectively, while there was a general decline in China.

Integrating Finance and Site Strategy

The build-or-buy decision sits at the intersection of finance, operations and location intelligence. Beyond site selection, it’s fundamentally about deploying capital effectively — balancing acquisition cost, modeling different scenarios, construction timelines and long-term scalability.

From our advisory work, investors face recurring challenges when acquiring in Asia:

- Valuation gaps due to differing accounting standards;

- Limited transparency in target company records;

- Family-owned business complications/succession issues;

- Complex approval processes for foreign ownership, especially in sensitive industries.

For example, in 2024, several foreign consumer-health groups opted for joint ventures or partial acquisitions to overcome regulatory barriers while gaining brand presence.

A Choice That Reveals Your Strategy

Ultimately, the path you choose says a lot about your company’s ambition and appetite for risk. Are you racing for market share? Then buying might be your best first move. Are you building a legacy asset for the next decade? Then building from scratch could be the answer. The good news is it is not an either-or choice. Many successful companies with available capital — what investors call “dry powder” — end up doing both, often starting with an acquisition to establish a beachhead and then building new facilities to scale.

In today’s regionalized, post-pandemic world dealing with complicated trade challenges and geopolitical issues, the ability to blend both models may be the pathway to successful Asian expansion.

Tractus is one of Asia’s leading strategic advisory firms assisting multinational companies to make informed investment decisions across emerging markets. Visit tractus-asia.com.