Two reports from OCO Global highlight top locations for global business services and shared services centers.

By special arrangement with OCO Global, a Northern Ireland-based advisory firm

specializing in global trade and investment, Site Selection here presents findings from “Next-Gen Locations: North America’s Future GBS/SSC Destinations.” The report was

released in June 2025 and co-authored by OCO Global’s Global Head for Site

Selection & Location Advisory Loïc Blanc with Manager Site Selection & Location

Advisory – U.S. Market Abby Varas. Also presented here are findings from the firm’s

previous report on emerging GBS/SSC locations in Europe. — Ed.

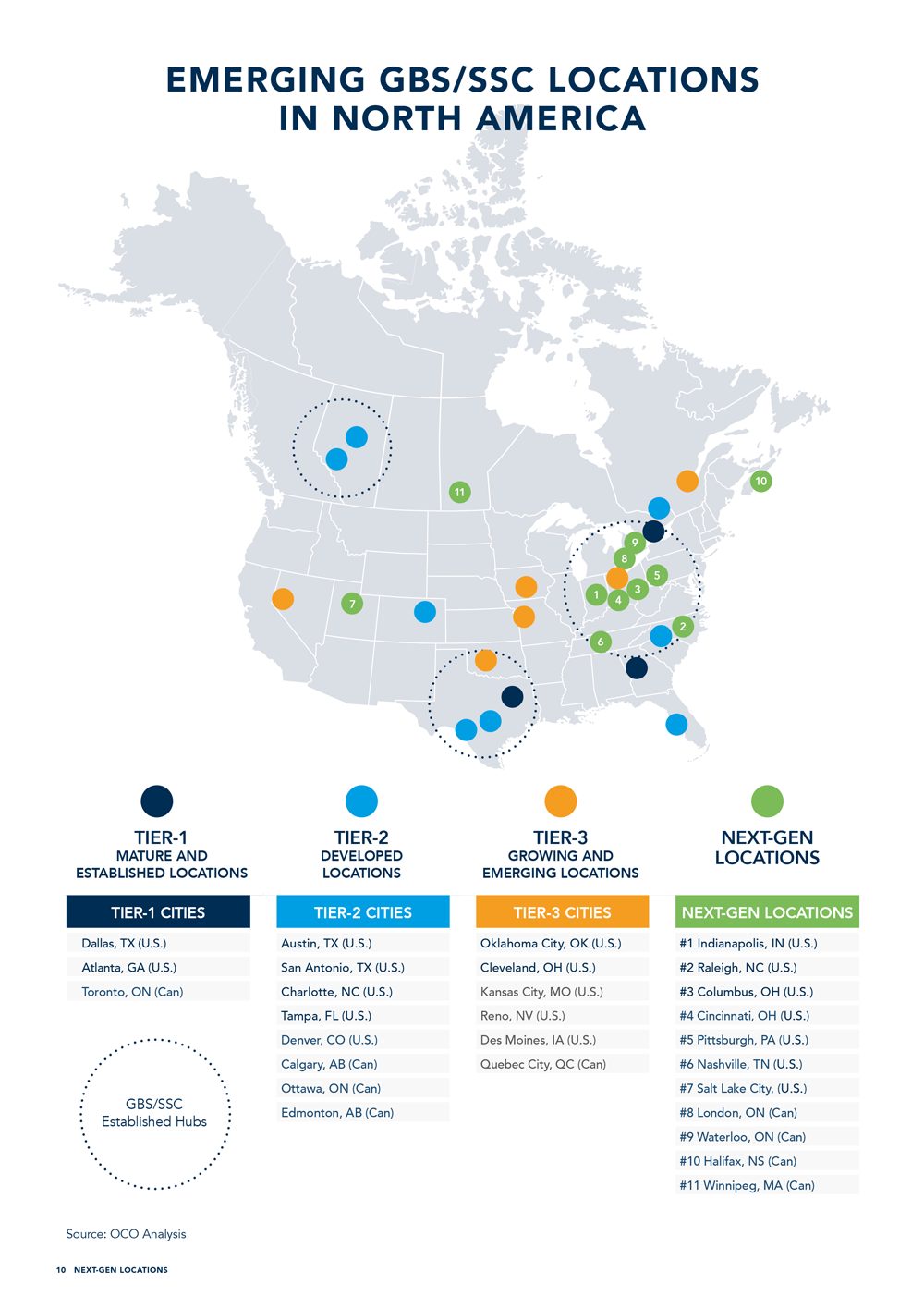

Building on the success of OCO Global’s first edition market report focused on emerging Global Business Services (GBS) and Shared Services Centers (SSC) locations in Europe, we now want to highlight opportunities in the Americas, home to nearly one-third of the global GBS market.

While Latin America has long captured headlines — with Costa Rica, Mexico and Colombia leading as dynamic and evolving hubs — this edition shifts the focus northward to the evolving landscapes of the United States and Canada.

A rapidly changing geopolitical environment is prompting a renewed interest in reshoring and localizing operations to core markets. This trend is gaining momentum in the U.S., where businesses are reassessing the balance between cost and quality.

At the same time, the growing adoption of advanced technologies — AI, automation and data analytics — has begun to reduce dependency on multilingual talent and transactional processes. As a result, strategic priorities are evolving from labor arbitrage to innovation, resilience and value creation.

In this context, we explore the rise of next generation (Next-Gen) locations across the U.S. and Canada, cities and regions that combine strong talent pipelines, innovation ecosystems, business-friendly environments and a readiness to support the future of GBS and SSC operations.

In today’s American SSC/GBS landscape, there is a strong concentration of activity in established hubs, with the U.S. accounting for 35% of respondents operating captive centers in these regions (SSON Report 2025). However, the unstable political environment, particularly since Donald Trump’s second presidency, introduced significant changes such as tariffs on trade, forcing businesses to reconsider their location strategies and become more responsive to the changing landscape to mitigate risks.

The search for best-available talent continues to drive multi-location models, complemented by cost savings, greater flexibility (particularly when leveraging suppliers) and enhanced productivity — especially within a “follow the sun” model.

Protectionist policies, such as the “America First” initiative, have encouraged companies to focus on onshoring rather than offshoring, particularly discouraging dependency on countries like China and India. The push to keep jobs onshore and ensure work is done within the U.S. further supports this trend.

This is paired with a deregulatory approach designed to ease the regulatory burden on businesses, fostering a more favorable environment for growth.

At the same time, there is a growing emphasis on technological investments, particularly in artificial intelligence, being applied across most functions as a means to increase pace of innovation, customer service quality, and back-office operation cost.

Looking ahead, upcoming federal elections in Canada and rising trade tensions between the U.S. and Canada add additional layers of uncertainty to the regional landscape. Potential policy shifts may affect cross-border operations, tariffs and investment decisions, requiring companies to remain agile and well-informed.

In this evolving landscape, it is a strategic moment for companies to review and adjust their location strategies, ensure they are diversified, and closely monitor changes in trade negotiations, policy and regulatory shifts, while also investing in automation and AI to stay competitive in a rapidly changing global environment.

“Over the past decade, GBS has expanded significantly, with many companies initially focusing on cost savings by offshoring to lower-cost countries like India, the Philippines, Mexico, and parts of Eastern Europe,” says award-winning GBS executive David Palmieri, who has over 30 years of experience in large-scale transformation at firms such as JPMorgan Chase, Citigroup, BNY Mellon, and Experian. “While this approach created growth, a ‘savings first’ mindset often led to challenges such as high attrition and reduced quality. Going forward, organizations are adopting a more balanced approach — cost remains important, but strategies are increasingly centered around talent, innovation and ecosystem strength.”

Asked which factors companies should consider when selecting next-gen locations, Palmieri says, “One of the most critical factors when choosing a next-gen GBS location is what I call the ‘sign on the door’ — in other words, what functions will the center perform, what scale of talent is needed, and which teams need to be collocated for collaboration. A GBS center focused on software innovation will look completely different from one supporting contact center operations or finance.

“Another key consideration is the operating model,” he says. “You need to think about the overall architecture — whether it’s a landlord model, the level of supplier involvement, contract types, remote versus onsite work, and the need for language skills. You also have to factor in how the location supports your employer brand. AI and robotics are no longer optional — they’re foundational. GBS organizations are now expected to innovate at scale, often through Centers of Excellence (COEs) that develop and deploy smart automation. These capabilities allow GBS to scale up without adding more people, essentially enabling 100% cost arbitrage. That opens the door to greater location flexibility. In some cases, it may even make sense to place parts of the COE in higher-cost markets if the benefits in speed and quality outweigh the cost.”

Instead of focusing on well-established hubs, which are often saturated and highly competitive, particularly in terms of talent, our approach targets next-gen locations: less mature markets that demonstrate significant growth potential. To identify those that might be under the radar today but are strategically positioned for long-term success, we scored and ranked cities based on the following drivers:

- Less mature markets (smaller population and labor force)

- High growth potential (population, labor force and GDP growth)

- Depth and maturity of the tech ecosystem (AI, automation, digital adoption)

- Future skilled talents (education system, availability of specific skills)

We then scored and ranked the locations to highlight overperforming tier-3 locations, both in the U.S. and Canada.

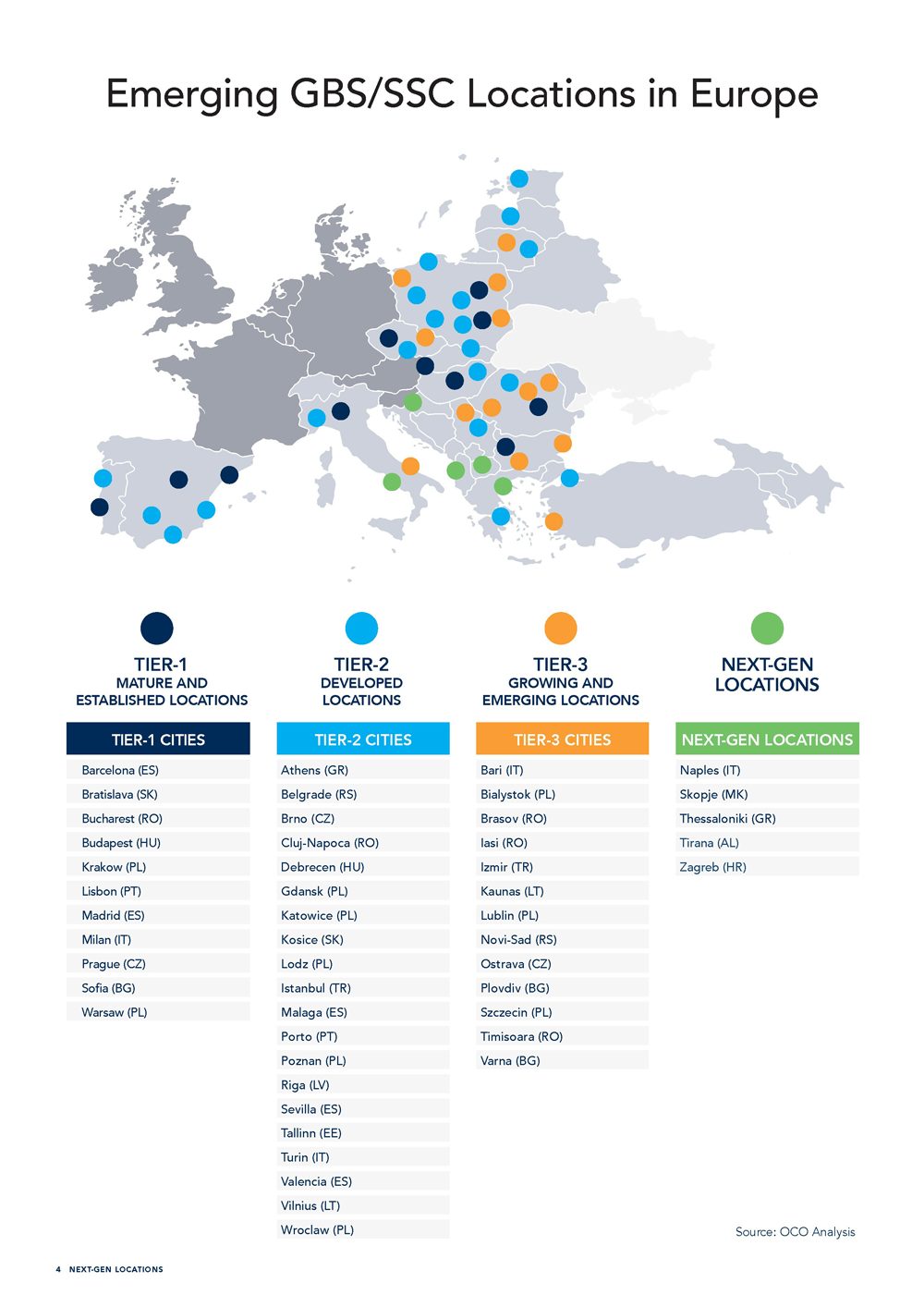

Location Decision-Making in a Changing Europe

Europe stands out as the world’s most diverse GBS market, boasting nearly 100 potential locations. Central and Eastern Europe has long been at the forefront, with Poland, Hungary and Czechia establishing themselves as key players since the 2000s.

The Baltics, along with Romania and Bulgaria, have also matured into well-regarded destinations known for their skilled workforce and competitive costs.

However, the region faces significant challenges that are reshaping its GBS landscape. Structurally, there is a growing war for talent, driven by low unemployment rates and increasing salary expectations, which is making historically attractive SSC/GBS locations less appealing. Moreover, since 2022, geopolitical tensions, particularly stemming from the Ukraine conflict, have heightened risk perceptions in these regions.

Consequently, Southern Europe has emerged as a compelling alternative, notably Portugal, which offers stability, a favorable business environment, and a growing tech ecosystem. Yet attention is also shifting toward newer locations within Europe. Countries like Spain, Greece, and Italy are increasingly capturing interest due to their strategic locations, skilled workforce and supportive government policies.

Moreover, emerging markets such as Macedonia, Georgia, and Albania are gaining recognition for their potential to become future GBS hubs.