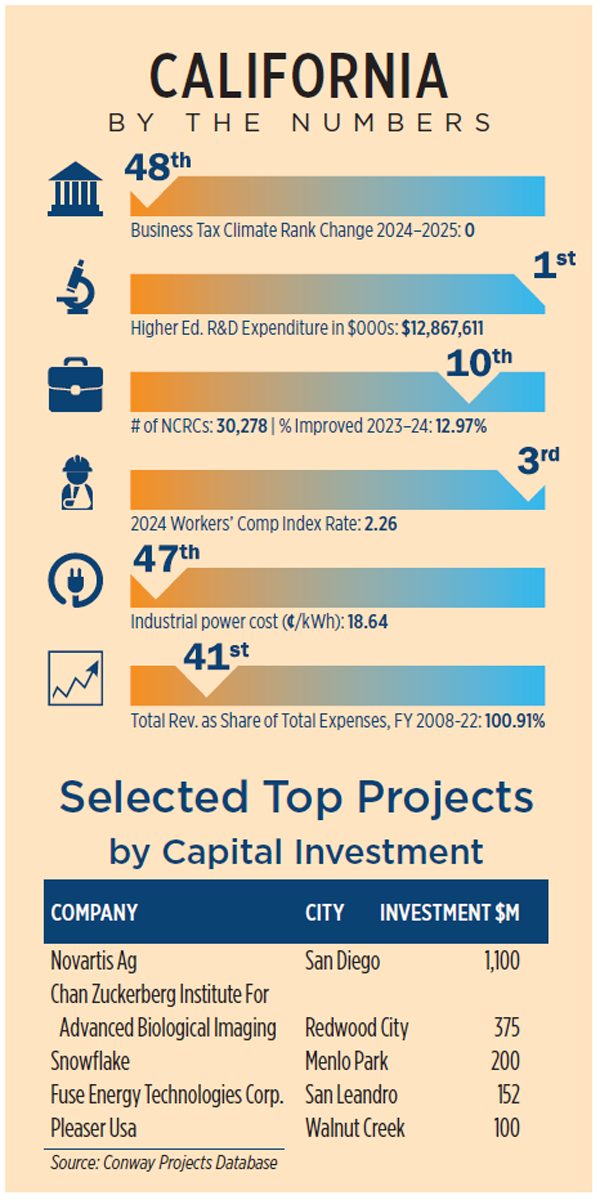

The Site Selection editorial team here takes on a state whose $4.1 trillion GDP, the International Monetary Fund determined in the spring, is the fourth largest in the world, ahead of Japan, India and the United Kingdom.

Why a $4 Trillion Company is Placing All Its Chips on Santa Clara

When the world’s most valuable company makes a bet that your community is the best place to build its global headquarters of the future, it’s safe to say that your area is winning. Welcome to Santa Clara, California, where Nvidia is investing nearly $1 billion into real estate acquisitions designed to position the company for sustainable, long-term success.

The artificial intelligence chip-making juggernaut with a market capitalization of $4.43 trillion as of August 13 has been on a property-buying spree the likes of which we haven’t seen in Northern California in a long time.

Santa Clara, a city of 134,587 people about an hour south of San Francisco, lies just west of San Jose in Santa Clara County, a Silicon Valley mainstay of 1.9 million people. Three of the largest microchip makers in the world — Nvidia, Intel and AMD — call this county home.

But it’s Nvidia that’s leading the charge into the AI-powered future of semiconductors. Nvidia’s graphics processing unit (GPU) has cornered the market of chips being used to drive the AI hyperscale data centers being developed and deployed worldwide. And right now, those digital infrastructure builders can’t secure Nvidia’s industry-standard microchips fast enough. Founded by Jensen Huang in 1993, Nvidia became the first company in history to surpass $4 trillion in valuation this summer.

Just two months ago, Nvidia filed plans to raze on old warehouse next to its Santa Clara HQ and replace it with a much larger office building. Nvidia intends to construct a 324,000-sq.-ft. office facility on this 11-acre site and add a parking garage with 3,000 spaces.

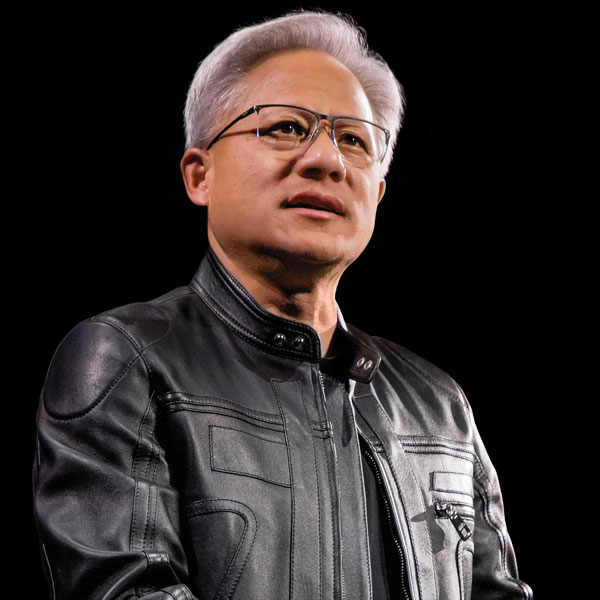

Jensen Huang, a graduate of Stanford University and Oregon State University, is founder, president and CEO of Nvidia, the world’s most valuable company.

Photo courtesy of Nvidia

The move comes months after Nvidia paid $124 million to buy a 10-building office park right before the company purchased an additional three office buildings near it for $339 million. Combined with Nvidia’s purchase last year of its own existing HQ campus from its landlord, the firm has spent approximately $836 million on real estate since May of 2024.

Nvidia completed construction on building two on its main campus three years ago. Altogether, the firm now occupies 1.25 million sq. ft. in the Endeavor and Voyager buildings in Santa Clara — built at a total cost of $370 million.

In various public statements, Nvidia has indicated that the new property acquisitions are designed to support the firm’s plans to invest up to $500 billion over the next four years into constructing AI supercomputers — and the firm says it will do all of this in the U.S.

Where AI Skills Congregate

Mark Muro, senior fellow at Brookings Metro, says that “Nvidia lies at the white-hot center of the global AI ecosystem and so it absolutely must remain in the nation’s superstar region of AI. AI skills, knowledge and scale-up are massively concentrated in the Bay Area, where the two main metros — San Jose and San Francisco — account for fully 13% of all job postings with AI skills. In terms of headquarters sitings, OpenAI, Anthropic and Databricks are in San Francisco, and Google, Nvidia and Apple are in Greater San Jose, making the region’s gravitational field irresistible for high-tech development and dealmaking.”

What sets San Francisco and Silicon Valley apart from all other metro areas in the country, says Muro, are AI-readiness assets. Nationwide, 14% of all online profiles of workers with AI skills congregate in these two metro areas. Other factors driving firms like Nvidia to cluster and expand in the Bay Area, he says, include:

- Eight percent of all federal AI R&D spending goes to the Bay Area.

- Nine percent of all AI publications and 34% of all AI patents go there.

- Stanford, University of California, Berkley, and other top schools are there.

- Fully 31% of all private AI startups founded after 2014 operate in these two metros.

- Thirty-two percent of total seed and early-stage VC funding for AI startups went to these two metros over the past two years, including the largest deal, valued at $10 billion, raised by San Francisco-based startup Databricks.

In light of these assets, says Muro, “it’s basically inevitable that Nvidia would pile onto its presence in the Bay Area. The place is in a class of its own for AI development and really there’s no other place for them to go in the U.S, even though we note several dozen quite impressive AI cities in our recent report on AI-ready metros. Nvidia’s needing to stay there and invest even more in Santa Clara reflects the special power of high-tech clusters, especially for emergent industries.”

120 Miles North, Sacramento Gets All A’s

Barry Broome, president and CEO of the Greater Sacramento Economic Council, says that Northern California is on an unprecedented roll. “When you look at the Greater Sacramento region — about 120 miles north of San Jose — we are among the 10 fastest-growing metros in the country, and we are seventh in job growth. We also have the top three locations for tech workers, according to LinkedIn; and we are rapidly moving up to become a top 10 town for semiconductors.”

He adds that Sacramento now has nine of the top 10 semiconductor companies in the world. “Rancho Cordova in Sacramento County is a hub for that sector,” he says. Bosch, for example, is investing $1.9 billion to convert its Roseville facility in nearby Placer County into the largest silicon carbide semiconductor production site among its global investments. The operation will create 1,700 jobs.

Blaize, a developer of AI computing solutions, went public earlier this year and raised $150 million. The El Dorado Hills-based firm was founded in 2010 by former Intel engineers and had raised a total of $335 million from investors before it went public.

And that’s not even Sacramento’s highest-profile win. That would be the former Oakland Athletics — now known as just the Athletics. For three seasons, this one-time American League powerhouse will play all of its home games at Sutter Health Park in West Sacramento. A recent three-game series against the San Francisco Giants sold out every seat and garnered national media attention.

Could that be a harbinger? Broome thinks so. “We have two objectives: Land a Major League Baseball team in 2028 and land a Major League Soccer franchise. Sacramento Republic FC has a huge following. We are building a $175 million soccer stadium in the rail yards. We think it should be home to an MLS team soon.” — Ron Starner

Life Sciences Reverberate Throughout the State

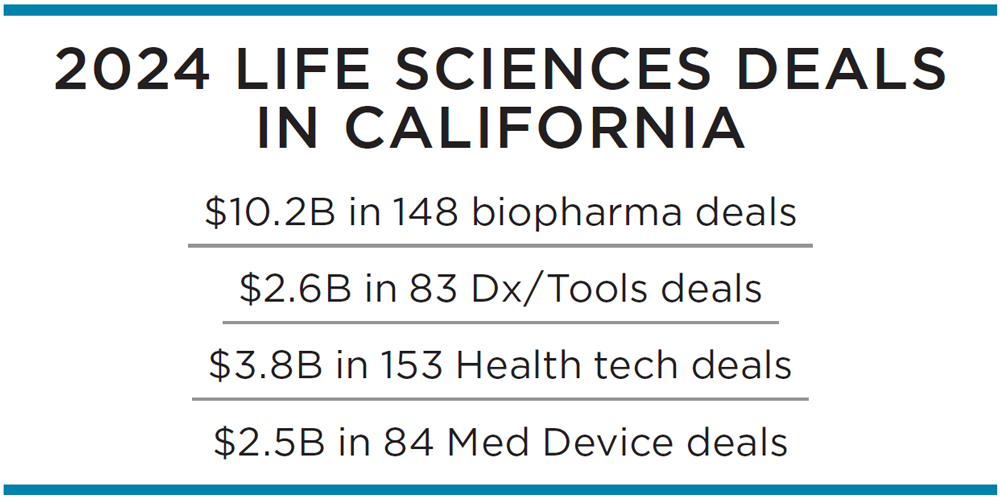

Fresh data revealed in Biocom California’s 2025 Life Science Economic Impact Report indicate many of the state’s metro regions are well poised to lead domestic and international life sciences R&D and manufacturing innovation.

Last year the industry contributed a $395.7 billion total economic output statewide, bolstered by over 17,220 life science companies supporting more than 1.15 million jobs, 452,445 of which are directly employed life sciences workers. Manufacturing-focused roles make up 31.2% of the state’s total life science workforce, ranking California above Massachusetts, New York, Pennsylvania and Texas.

Digital technology will play an important role in guiding fresh corporate investment. Deloitte’s survey of 150 C-suite executives revealed that almost 60% plan to increase deployment of generative AI into operations, which could create up to 11% in value creation relative to revenue within functional areas by 2030.

The Golden State Impact

The state’s $65.6 billion direct labor income impact in 2024, although impressive, could have been stunted by a 3.1% decrease in payroll employment which saw a loss of more than 14,400 jobs across the industry. Sub-sectors that experienced the brunt of layoffs were concentrated within areas such as pharmaceutical manufacturing, nanotechnology R&D, biotechnology R&D, medical laboratories and medical equipment wholesale. Each of the state’s leading life science regions, minus Orange County within manufacturing, saw a decline in overall employment during this time.

Regardless, sectors like surgical and medical equipment manufacturing, for example, helped offset these losses by adding over 1,000 new jobs over the year. New opportunities are on the horizon as 468 new project investments, totaling over $19.1 billion, were announced by biopharmaceutical, medical device, health tech and Dx/tools companies in 2024. As a whole, California’s life sciences industry drew in $63.1 billion in new investment deals. Some highlights for the year include:

- Switzerland-based pharmaceutical manufacturer Lonza invested $1.2 billion to acquire Genentech’s former large-scale biologics manufacturing facility from Roche, located in Vacaville, California. The company announced an additional $500 million would be used to upgrade the site to prepare for next-generation mammalian biologics therapies.

- As part of $23 billion in planned U.S. investment over the next five years, Novartis will construct a $200 million manufacturing facility in Carlsbad expand its radiopharmaceutical portfolio. The plant, anticipated to be complete by 2026, will be the company’s third U.S.-based radioligand therapy production facility. The company is also establishing its second global R&D hub in the U.S. in San Diego, a $1.1 billion investment.

Biocom’s report notes that California’s life sciences industry is driven by six major sectors including biotechnology, biopharmaceuticals, medical devices and equipment, research and testing, scientific research tools and food and agriculture biotechnology. Dominance within these areas is reinforced by a steady stream of research funding. Of all U.S. states, California receives the most National Institutes of Health (NIH) and National Science Foundation (NSF) funding, pulling in a combined $5.7 billion across 10,624 awards in 2024.

Regional Insights

The Bay Area’s nine counties — Alameda, Contra Costa, Marin, Napa, San Francisco, San Mateo, Santa Clara, Solano and Sonoma — continue to serve as the nucleus of California’s life sciences industry, leading with a $123.6 billion total economic output in 2024.

A closer look at the county-level economic impact shows that San Mateo County ($50.3 billion), Santa Clara County ($29.6 billion) and Alameda County ($25 billion), led the region in total output activity. Nearly 150,500 of the state’s industry employees are located in the Bay Area, a majority of which are employed within biotechnology, research and testing and biopharmaceutical sectors. These counties hold over 3,800 life sciences operations. Industry leaders located throughout the region include Abbott Laboratories, Bayer, Intuitive Surgical, Johnson & Johnson, Genentech and Thermo Fisher Scientific.

Top research institutions University of California San Francisco; Stanford University and University of California, Berkeley, are a powerful pull to the Bay Area, churning out an array of diverse talent. The region’s prime research capabilities made it the beneficiary of $2.15 billion in NIH and NSF funding over the year.

Greater Los Angeles was the second-highest-performing California region in 2024, contributing a $60.2 billion total economic output. It actually tops the Bay Area in the number of life science establishments with over 3,966 in the region, portfolio toppers Amgen, Grifols, Kite Pharma and Takeda among the major employers.

University of California San Francisco is one of several universities that help the Bay Area lead in talent and in R&D.

Photo by Barbara Ries courtesy of UCSF

San Diego follows with a $54.1 billion 2024 economic output impact. The region holds over 72,300 more employees than Greater Los Angeles at 166,907 workers. Direct employees total 71,448 among the region’s 2,042 life science companies.

The research and testing sector holds the highest concentration of regional talent as several major life sciences companies have located R&D centers here, including Bristol Myers Squibb, Eli Lilly, Hologic, Pfizer and Vertex. — Alexis Elmore

Rockets Over California

California is home to one-third of all U.S. space tech startups and is also the recipient of over 70% of venture capital space tech funding in the country, having received $60.8 billion in defense contract spending in 2023 and generated over 66,200 jobs, $18.5 billion in economic output and $1 billion in state tax revenue.

Coined “Space Beach” for its long-standing reputation as a major aerospace & defense (A&D) hub, Long Beach has also welcomed the operating locations and headquarters of several companies such as JetZero, Rocket Lab and Boeing. In early 2025, Colorado-based aerospace & defense technology company True Anomaly Inc. revealed it would also call Space Beach home with a 90,000-sq.-ft. facility that will include a 20,000-sq.-ft. office space.

“Long Beach is the perfect location to usher in a new era of space defense, and we’re thrilled to establish an epicenter of defense disruption there,” says Even Rogers, True Anomaly CEO and co-founder. “At a time when space is the most promising physical frontier for human exploration as well as an emerging battlefield, our new campus gives us an important edge. The local aerospace ecosystem will allow us to accelerate the design and production of breakthrough technologies that address dynamic new threats on orbit. This expansion sets the stage for True Anomaly to lead in securing and advancing humanity’s next great arena.”

The space defense company recently closed on $260 million in an oversubscribed round of series C financing that aims to accelerate vertical integration, facility expansion and product development.

Site Selection spoke with Emily Desai, chief deputy director at the California Governor’s Office of Business and Economic Development (GO-Biz), about the A&D industry in California. — Kelly Barraza

What makes California so attractive to A&D companies?

Emily Desai: California’s aerospace & defense sector benefits from a combination of assets — a highly skilled workforce, existing infrastructure, expansion opportunities and a long history of innovation. Employing over 115,000 workers, California is home to 16% of the national A&D workforce, which is the largest share in the United States. The state is also home to a strong pipeline of talent supported by industry-led training programs and top-ranked institutions, including the California Institute of Technology and Stanford University — two of the top three aerospace engineering universities.

Furthermore, the Golden State’s robust infrastructure includes leading research centers, test ranges, rocket engine facilities and key NASA and Department of Defense installations, supporting everything from design and development to testing and launch.

With over 1,900 aerospace & defense companies, California offers the opportunity to build strong B2B relationships and collaborate on large defense contracts, creating a robust network for state and local partnerships. California’s proximity to NASA and defense also positions the state as a desirable opportunity for A&D companies to partner and share capabilities — in 2023 alone, NASA procurement investment totaled $5.8 billion in California, with $2.1 billion going to California businesses.

The major A&D hubs in California are Los Angeles, San Diego, Palmdale, El Segundo and the Bay area. Are there any other cities in the state where the industry is growing?

Emily Desai: California’s Central Coast, anchored by the Vandenberg Space Force Base and UC Santa Barbara, has become a growing hub for aerospace & defense, with an expanding ecosystem of hard-tech companies and a network of businesses critical to national security and space. This region forms a key piece of California’s space triangle — manufacturing in Los Angeles, testing in Kern County and launching from Vandenberg. With Monterey and Ventura counties hosting companies developing electric Vertical Take-Off and Landing aircraft (eVTOL), the Central Coast is also emerging as a leader in advanced air mobility (AAM).

Orange County and the Inland Southern California regions also have an established base of tier 1 and 2 suppliers to aerospace & defense. Robust talent pipelines, proximity to workforce and site availability have made these regions attractive for A&D vendors. Lastly, the Greater Sacramento region has a convergence of precision manufacturing activities that have fed the aerospace industry. The region’s concentration of A&D precision manufacturing jobs is approximately 1.75 times the national average.

What kind of programs or tax incentives does the state provide to A&D companies?

Emily Desai: Over the last 13 years, the Governor’s Military Council has helped position California to maintain and grow operations in the state, inclusive of the A&D industry. Within the last few years, Governor Newsom wanted to ensure a more targeted focus and launched the California Space Industry Task Force to attract A&D businesses, expand research and development and create models for public/private cooperation.

In the recently released California Jobs First State Economic Blueprint, “Space, Defense, and Satellites” was named as one of four pilot sectors that will receive strategic support from the state. Accordingly, GO-Biz has launched a working group comprising state agencies with purview in the space sector and regional economic development representatives to continue the advancement of this industry. As a part of this workstream, five of the 13 Jobs First Collaboratives that identified aerospace & defense as a regional strategic sector — the Bay Area, Central Coast, Los Angeles County, Kern County and the Southern Border Region along with Orange County and Inland SoCal — are contributing to the Space Working Group efforts.

Other key state-wide incentive programs are as follows:

- The California Competes Tax Credit (CCTC) is a corporate income tax credit for companies looking to create jobs and investments in California.

- The California Investment Incentive Program provides a complete property tax abatement for large investments in manufacturing (including aerospace & defense) when capital investment exceeds $25 million.

- The California Space Flight Property Tax Exemption exempts qualified space flight property (satellites, space vehicles, launch vehicles and fuel exclusively for space flight) from property taxes.

What are some examples of A&D projects that state tax money helped support?

Desai: Earlier this year, Uplift Central Coast awarded a $550,000 grant to the County of Ventura’s Economic Vitality Unit to create an Advanced Air Mobility (AAM) Innovation Center at the Camarillo and Oxnard Airports. The planned Innovation Center will feature a 500-square-mile testing range for AAM at the airports, which are both operated by the County of Ventura, as well as research facilities, business resources and workforce training opportunities. Since 2019, the state’s CalCompetes program has awarded just under $230 million in tax credits and grants to aerospace-related companies.

Recent highlights include Relativity Space leasing a former Boeing facility in Long Beach and commiting to creating over 1,000 new jobs there and at their second launch site at Vandenberg. This 1-million-sq.-ft. Long Beach facility has the largest 3D printers in the world, which will produce the full-scale space technologies necessary to make a Mars mission possible. CalCompetes also provided Astra with the capital needed to expand both manufacturing and research & development capabilities at their facility in Alameda that has over 330 full-time employees.

Where California Is Pulling Its Industrial Output Weight

Recent analysis from the Information Technology & Innovation Foundation (ITIF) reveals good news for the Golden State. Its May 2025 State Hamilton Index ranks California fifth in the U.S. for overall industrial performance in terms of output across seven industries. They are IT and Information Services; Electrical Equipment; Motor Vehicles; Machinery & Equipment; Computers, Electronics & Optical Products; Other Transportation; and Pharmaceuticals and Biotech. Each category includes one or more subindustries, bringing the number of sectors scored to 21.

The Index, authored by ITIF’s Meghan Ostertag, quantifies states’ innovation-driven production relative to China’s performance in the same context. Why? Perhaps as a wake-up call to the 50 states to do better at pulling their production-output weight where possible.

“Innovation-driven production is key to reclaiming U.S. dominance on the international stage,” notes the report’s introduction. “Once the leader in the production of advanced technologies, the United States now finds itself with less capabilities than the global average. Over the past several decades, the erosion of domestic industry has slowed economic growth, weakened the terms of trade, degraded national security and made America vulnerable to China’s innovation mercantilist tactics.”

What’s Your LQ?

The State Hamilton Index is based on a location-quotient (LQ) system with an LQ above 1.00 indicating output overperformance in an industry or subindustry and a score below 1.00 indicating underperformance. Nineteen states have overall LQs above 1.00; California’s 1.38 is fifth nationally.

The state’s performance — or overperformance, more accurately — in three of the Index’s seven broad industries is behind its fifth place ranking overall. Its LQ in Pharmaceuticals and Biotech is 1.67. Its LQ is 1.49 in IT and Information Services and 1.39 in Computers, Electronics & Optical Products. Underperformance characterizes the other four industries in California’s case with an LQ of 0.33 for Motor Vehicles being its weakest output contributor.

Drilling Down

Here’s how California stacks up in the subindustries comprising the three main industries in which it shines:

Pharmaceuticals and Biotech (1.67): Nineteen states overperform in Pharmaceutical and Medical Manufacturing, including California with its 1.22 LQ; 15 states have higher LQs. It does better in Biotechnology R&D with a 2.58 LQ, the fourth highest nationally.

IT and Information Services (1.49): California is one of just 10 overperforming states in Software Publishing, placing fifth nationally with an LQ of 1.93. In the Data Processing, Hosting and Related Services subindustry, its 1.27 LQ is in 10th place in a three-way tie with Maryland and Georgia. California’s 3.38 LQ for Internet Publishing, Broadcasting and Web Search Portals is the clear winner with the second place state at 1.78.

Computers, Electronics & Optical Products (1.39): Nineteen states also overperformed in the Computer and Electronic Manufacturing subindustry with California’s 1.39 LQ placing 14th nationally. No other subindustries are included.

ITIF’s State Hamilton Index includes policy recommendations for states, one of which is to “Stop Using Taxpayer Dollars to Attract Chinese Companies to the United States,” which would help level that playing field by making businesses in innovation-driven sectors in California and all states more competitive.

— Mark Arend

State Makes Headway with Apprenticeship

At this writing in August, there are 92,588 registered apprentices in California, according to the California Department of Industrial Relations (DIR), which will celebrate its 100th anniversary in 2027. Another 1,200 are registered trainees and another 4,000+ are registered pre-apprentices.

But those numbers are only signposts on the journey to what Governor Gavin Newsom envisions: 500,000 apprentices served by 2029. Since 2019, California has served 215,393 registered apprentices, according to the DIR’s Division of Apprenticeship Standards (DAS).

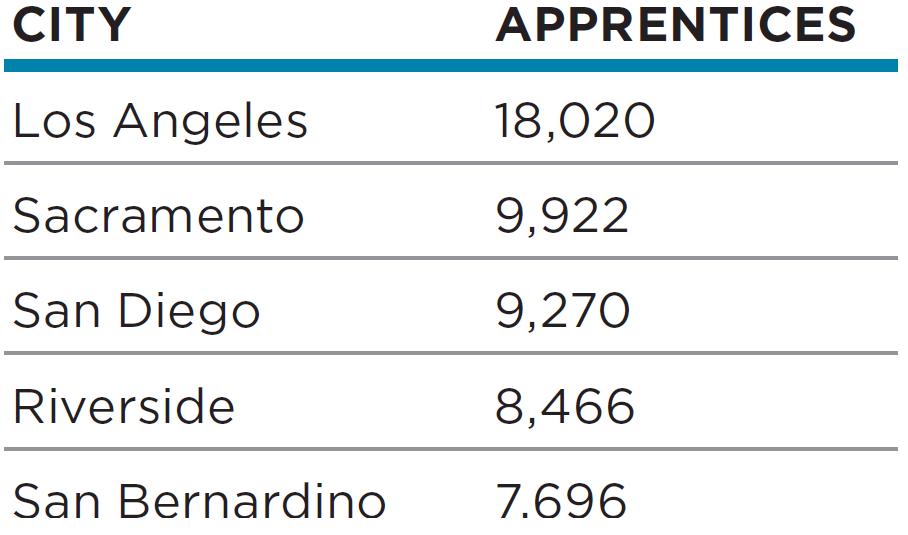

The DAS provides a breakdown of apprenticeship data by industry and by county that can be helpful to companies scouting locations and scouting talent. Top fields are firefighting (12,239), carpentry (10,426) and electric/electronics (7,721). By county, here are the top five in terms of overall apprentices of every stripe:

Gov. Gavin Newsom

Since the beginning of the year the state has announced nearly $130 million in funding to support apprenticeships, including two tranches in July and August that dedicate $20 million toward apprentices in the building trades to fill infrastructure jobs (a seven-fold increase over previous years’ allocations) and another $26 million to support women apprentices in construction. (The state’s total of all women apprentices across all fields only comes to just over 10,300.)

National statistics from the U.S. Department of Labor differ slightly. As of FY 2025 the DOL’s Registered Apprenticeship Partners Information Database System (RAPIDS) tallied 80,846 apprentices residing in California. But any way you slice it, the state is No. 1 by a country mile. The next highest numbers are in Texas, where the total of 36,822 is less than half of California’s, and in Ohio (25,279). California’s apprentice cohort — supported by a network of partners that include the state’s 116 community college campuses — represents 12% of the national total of more than 678,000. — Adam Bruns