In the last five years, the number of operational rail services on the New Silk Rail Route between China and Europe has grown to about 150 rail shuttles per week. These rail container shuttles connect over 30 European cities with 16 regions in China. Are these regular rail services between China and Europe here to stay in the coming years? What is the impact on the services of the COVID-19 pandemic? And are there any new site location trends in Europe?

Economic, logistics and real estate consulting firm BCI Global recently carried out a study into the current use and future potential of the New Silk Rail Route between China and Europe. The study was co-sponsored by LOGISTIS, a fund managed by AEW, one of the largest investors in European logistics real estate.

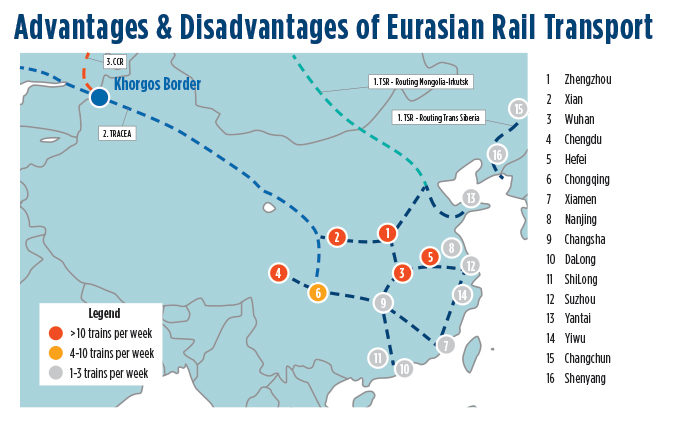

The rail route is part of the larger-scope Belt and Road initiative launched by China five years ago, which also includes a “Maritime Silk Road” element connecting through Malaysia, Indonesia and Singapore; India; eastern Africa and the Middle East, connecting to Europe in Italy.

Advantages

+ Rail is the shortest connection between western China and production locations in Eastern Europe.

+ Rail is positioned between sea and air cargo in terms of cost and lead time.

+ Shippers have had good experiences in terms of reliability.

+ Rail has proved to be a trustworthy alternative to sea and air.

Disadvantages

– Transport costs are relatively high compared to sea cargo (the default transportation mode for shippers).

– There is increased congestion risk due to limited capacity and bottlenecks in the network.

– Transparency and visibility of rail transport need to be improved.

– LCL services and direct deliveries via rail need to be improved.

In the last 10 years, the 9,000 kilometers of rail infrastructure between China and Europe has been improved substantially. In 2006 it took more than 30 days for a rail container shuttle between China and Europe, but nowadays it takes 14-18 days. This is due to improvements in physical infrastructure as well as operational handling and administrative procedures on the New Silk Rail Route. In turn, this has led to a steady increase in the use of the New Silk Rail Route for containers. In 2019, a total of 347,000 TEUs were shipped by rail between Europe and China, while 380,000 TEUs were shipped in just the first eight months of 2020.

With this increase, rail transport has become a solid third transport alternative next to existing sea and air transport connections for mid- to high-value and time-critical goods. COVID-19 has a major influence on the operational use of all three modalities, but the numbers show that the use of the New Silk Rail Route has steadily grown in 2020.

In mid-2020, operational users of the rail connections between China and Europe were interviewed about their experiences with rail transport between China and Europe. Seventeen international shippers responded from the automotive, machinery and electronics industries, which are the three industrial sectors with the highest rail volumes on the Eurasian rail route in past years. Additionally, the insights and experiences of 13 logistics services providers which offer Eurasian rail shuttle services themselves or are acting as forwarding companies for international manufacturers were gathered.

Rail as Third Way

The COVID-19 pandemic has had a substantial impact on the operational use of the New Silk Rail Route in 2020. In the first months of 2020, China experienced a lock-down and production facilities were closed, while in the spring Europe had its first lock-down. At the end of 2020, many European countries are again in lock-down. This all had impacts on both production volumes and customer buyer behavior, next to other trends.

Automotive shippers expressed their caution concerning the market development in 2020 and the near future, because the COVID-19 pandemic increased the uncertainties in the dynamic global market. However, all shippers also indicate that Eurasian rail transport is becoming a solid third transport alternative next to sea and air transport. International air transport had been hit especially hard by the COVID-19 pandemic, with many belly freight connections canceled. Also, the sea transport market has seen much upheaval, with sailings being partially or completely canceled. Global sea container freight prices have also doubled in the last six months. Shippers are now increasingly using all three transport modes, but the vast majority of the volume (94% in 2019) is still going by sea transport.

All these developments have resulted in a steady rise in Eurasian rail transport volume in the past 12 months, especially to and from destinations in inland China. The logistics service providers report that the client base among shippers for the New Silk Rail Route has broadened. They see growing opportunities and plan to improve the rail product (services, better planning, new connections). The main reasons for the increased interest are the shorter and more reliable transit time of rail transport compared to sea transport, and the competitive price for transport if traveling to and from inland China destinations.

In addition to the westward bound volume to Europe, the eastward-bound volume has risen due to the trade imbalance and subsequent low prices. However, the competitive position of China-Europe rail transport is for now partly depending on the subsidies for Eurasian rail transport that are granted by the Chinese authorities. These subsidies could go down in the coming years, but the Eurasian rail transport market will also become more mature.

Will the rise of Eurasian rail transport have an impact on future site selection strategies of international shippers and logistics service providers? BCI Global sees increased interest in some European locations.

Duisburg, Germany. is the main rail hub for the New Silk Rail Route in the European network and offers good accessibility to the biggest markets and main ports. Rail terminals in Polish cities Poznan, Warsaw and Lodz function currently as a rail hub locations for the connections to Central and Eastern Europe. Dobra in Slovakia resolves one of the major gauge bottlenecks for entering the EU market from China via rail. The market volume is still small but there is growth potential.

Minsk in Belarus strengthened its hub function for the connections to the Baltic states and Scandinavia, due to increased rail terminal investments. Kiev in Ukraine has an opportunity to become a regional hub in far Eastern Europe.

In China, about two-thirds of all rail shuttles in 2020 originated from three cities in inland China: Xi’an, Chongqing and Chengdu. These three cities are interesting centrally located rail hubs.

The research study shows that the Eurasian rail transport market is developing in terms of both volume and quality of services, and continues to grow in a dynamic way during the COVID-19 pandemic. The share in total China-European trade is still limited. But the expectation is that the Eastern European locations and inland China rail hubs mentioned will gain interest, particularly from logistics services providers who have a strong focus on Eurasian rail transport.

Based in the Netherlands, BCI Global carries out research, advises, implements and performs project management in the areas of supply chain strategy and design, international business strategy, location search and site selection, regional economic development, real estate and logistics. For more, visit bciglobal.com.