Optimism & Opportunity In Europe’s Office Sector

by Sukhdeep Dhillon, Head of EMEA Forecasting, Cushman & Wakefield

editor@siteselection.com

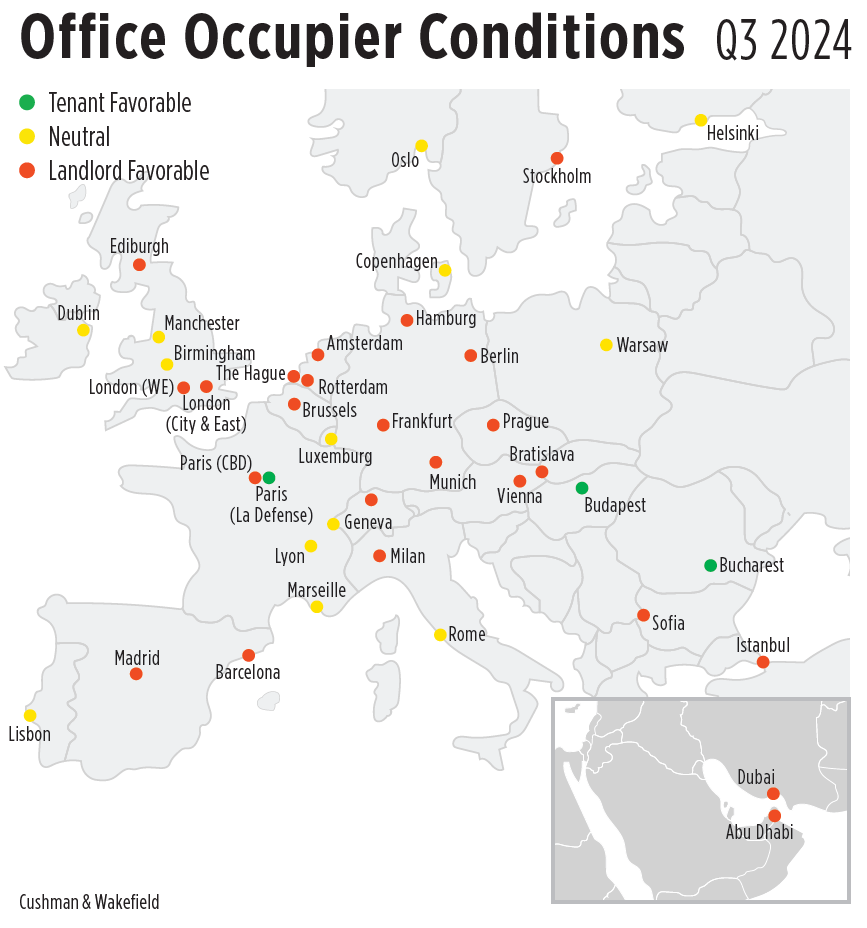

The improving economic environment is playing a key role in shaping the office market’s outlook. As economic growth strengthens and business sentiment improves, companies are increasingly confident about their long-term prospects. This confidence is translating into higher demand for office space, particularly in core markets like London, Paris, and Madrid.

In the first three quarters of 2024, 7.4 million square meters (more than 79.6 million sq. ft.) of office space was leased across Europe, marking a 3% increase over the same period in 2023. More than half of Europe’s markets — including key cities like London, Brussels, Madrid, and Barcelona — saw growth in leasing volumes.

One of the key trends in the office leasing market is the flight to quality. Companies are increasingly seeking Grade A office space — modern, well-located buildings offering top-tier amenities and energy efficiency. In fact, Grade A leases now account for over 50% of leasing activity in major cities, up from just over 40% in 2019. This shift highlights how businesses are prioritizing high-quality office environments to support employee well-being, attract top talent and help achieve corporate ESG commitments.

“Sustainability and carbon reduction are increasingly vital in the office sector, driven by the EU’s Energy Performance of Buildings Directive (EPBD), which sets higher energy efficiency standards as part of the push toward net-zero emissions.”

Balancing Quality and Costs

However, tenants are also becoming more cost-conscious, balancing the desire for premium office space with the need to manage rent expenses. Prime office rents are expected to rise by an average of 4.4% in 2024, slightly down from 5.7% in 2023. While rent growth is slowing, demand for prime office space remains strong, particularly in key cities where availability is limited. As businesses recover and expand, the demand for high-quality office space is expected to continue to grow, though tenants will likely seek ways to mitigate costs where possible.

Strong demand for prime office space is expected to support rent growth in the short term. However, new office completions, expected to peak at 5 million square meters (53.8 million sq. ft.) in 2024, will likely contribute to rising vacancy rates across all grades. While vacancies will increase due to the influx of new developments, most of the space being completed is in prime locations, where demand remains high. As a result, vacancy rates will likely remain lower in sought-after areas, while older, less efficient buildings may see higher vacancies.

Sustainability and carbon reduction are increasingly vital in the office sector, driven by the EU’s Energy Performance of Buildings Directive (EPBD), which sets higher energy efficiency standards as part of the push toward net-zero emissions. Property owners, especially those facing lease events soon, must prepare for these changes, as they could impact asset values, leasing terms and tenant demand.

Additionally, climate risks like rising temperatures and extreme weather are influencing the future of office real estate. Property owners must evaluate how these factors affect portfolio resilience and long-term value. With growing emphasis on environmental responsibility, energy-efficient and climate-resilient buildings will be in higher demand.

As tenant preferences evolve, the market is seeing a shift toward higher-quality, flexible office spaces. Landlords are responding by repositioning and refurbishing older buildings to make them more attractive to tenants. This trend is particularly noticeable in major cities like London and Paris, where older office buildings are being renovated to meet modern demand.

In some cases, older buildings in peripheral areas may face declining demand. As tenants seek newer, more efficient office space in prime locations, older buildings may become obsolete. This could lead to a rise in repurposing older office stock for alternative uses, such as residential or mixed-use developments. Repurposing will become an increasingly viable solution in locations where traditional office space is in low demand, especially in non-central areas.

Repositioning older office buildings and investing in sustainability will be key to maintaining competitiveness in the evolving market. The trend of upgrading and enhancing older properties is expected to continue, as landlords seek to align with changing tenant needs and environmental requirements.

As investors and tenants navigate these evolving trends, proactive strategies focused on sustainability, climate resilience and high-quality assets will be essential for long-term success. The office market is poised for steady recovery, with significant opportunities for those prepared to adapt to the changing landscape.

Economist Sukhdeep Dhillon, based in the United Kingdom, heads the Cushman & Wakefield EMEA forecasting team, which provides real estate forecasts and analysis for 119 prime markets spanning 22 countries.